The Air Traffic Picture: Let’s Tumble To Reality

When The Destinations Are Closed, Nobody’s Going To Travel

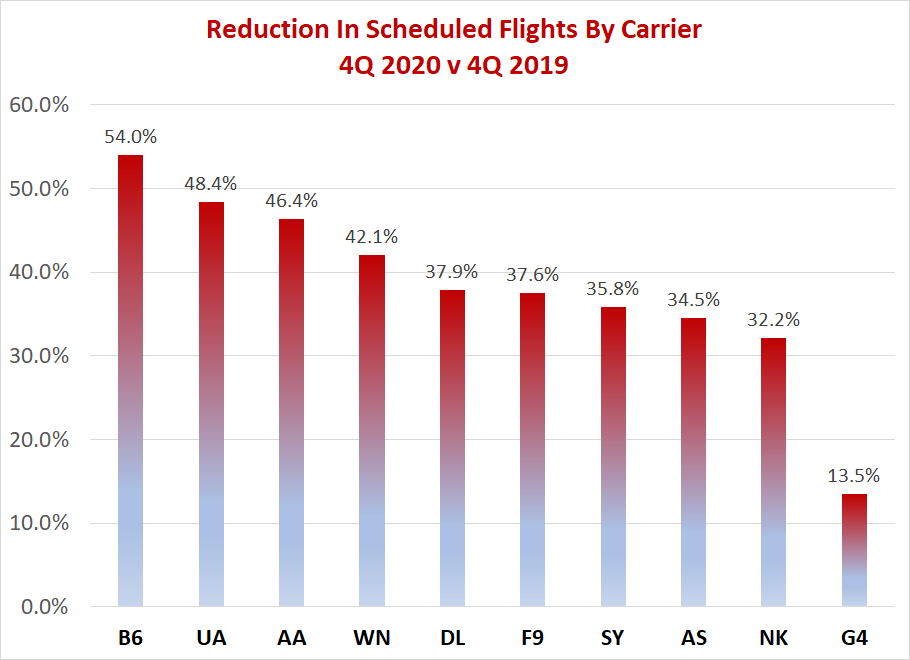

There have been some positive signs in regard to certain airlines restoring some hub-feed markets.

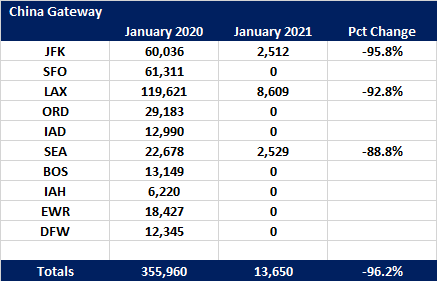

But on the wider picture, things are not so rosy. The China-CCP pandemic is still winning.

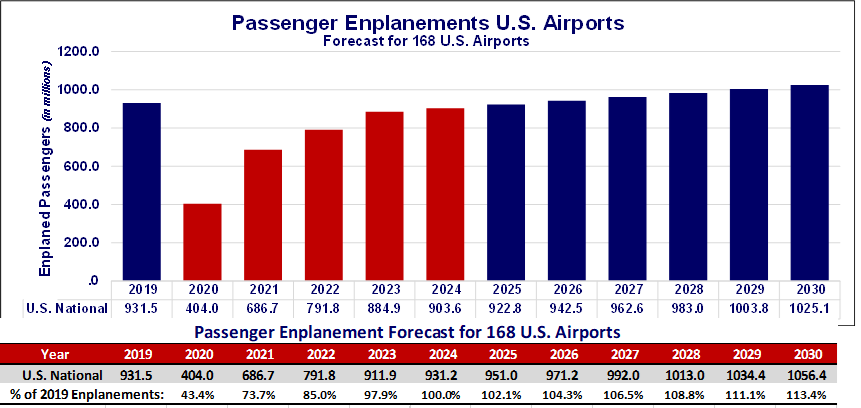

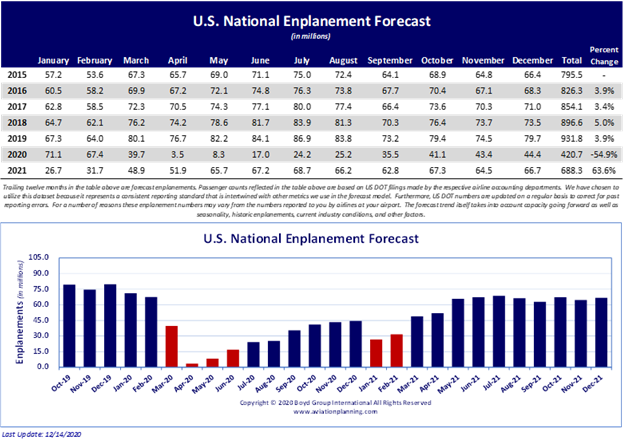

The latest iteration of the Airports:USA national short term forecast indicates a very steep plunge in enplanements for January, February and maybe March.

It is not rocket science. It’s due to uncontrolled chaos, really.

It is not rocket science. It’s due to uncontrolled chaos, really.

When Los Angeles is closed up like a giant economic clam, when the Mayor of New York is running in circles closing restaurants and decrying the fact that sane people are leaving the city in droves, when national politicians who aren’t doctors (but play one on TV) demand masks for everybody everywhere, this is not a situation that engenders a lot of hankerin’ to fly someplace.

Even the medical industry is chasing its tail. When the AMA suddenly retracts it’s across the board condemnation of hydroxychloroquine, and is now encouraging the use of the 65-year old drug (no longer politically tainted, apparently) it is very clear that the entire handing of this China virus is a giant panic run. Or, maybe more accurately, a political run.

The hard fact is that all this stuff discourages and actually prevents people from using air transportation. So, the only option for airlines is to pull back capacity. Actually, it’s not the virus, but all the confusion and political shenanigans surrounding it.

Get Ready For A January Surprise. The Airports:USA forecast for January indicates about 44 million fewer national enplanements in January compared to last year. The assumption is that the vaccines being delivered as a result of Operation Warp Speed will re-establish some semblance of confidence among public officials.

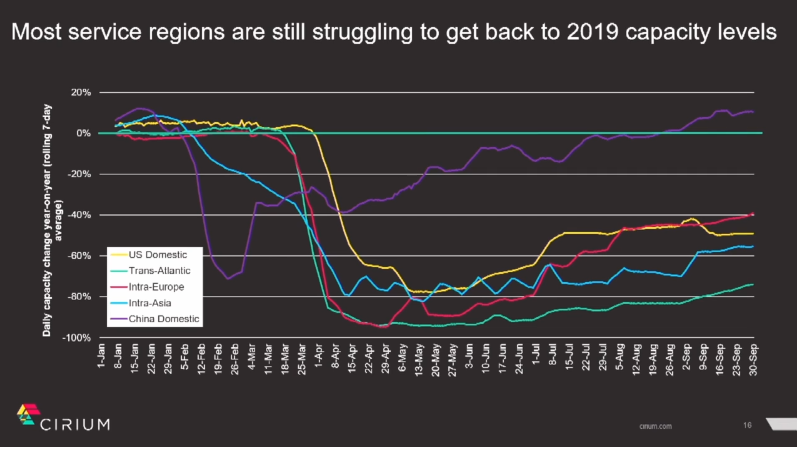

International Travel: Not Coming Back In 2021. Unfortunately, this is still a global air transportation mess. Australia is essentially air-service shut. Canada-U.S. border is closed, and even travel between provinces can have severe restrictions. (What’s another mystery of political fog, while Canada is being hamstrung by the China virus, the government is discussing joint military training with Canadian and Chinese troops. (Earth to Ottawa, come in please.)

And From The Coronavirus Motherland... As if there is any justice in the world, the CCP-China virus is still spreading across China, where the CCP six months ago claimed it was completely stopped. ‘Course, they are only reporting a few cases, here and there, don’t ya know. Plaid-jacketed con men at second-tier used car lots are pikers compared to these guys.

Not to worry, the CCP – the Chinese Communist Party – (the unelected life forms that run China) has announced that it and the World Health Organization are going to team up to find out really, really, where this virus actually came from.

Now, there’s a real powerhouse of integrity to bet on.

_______________

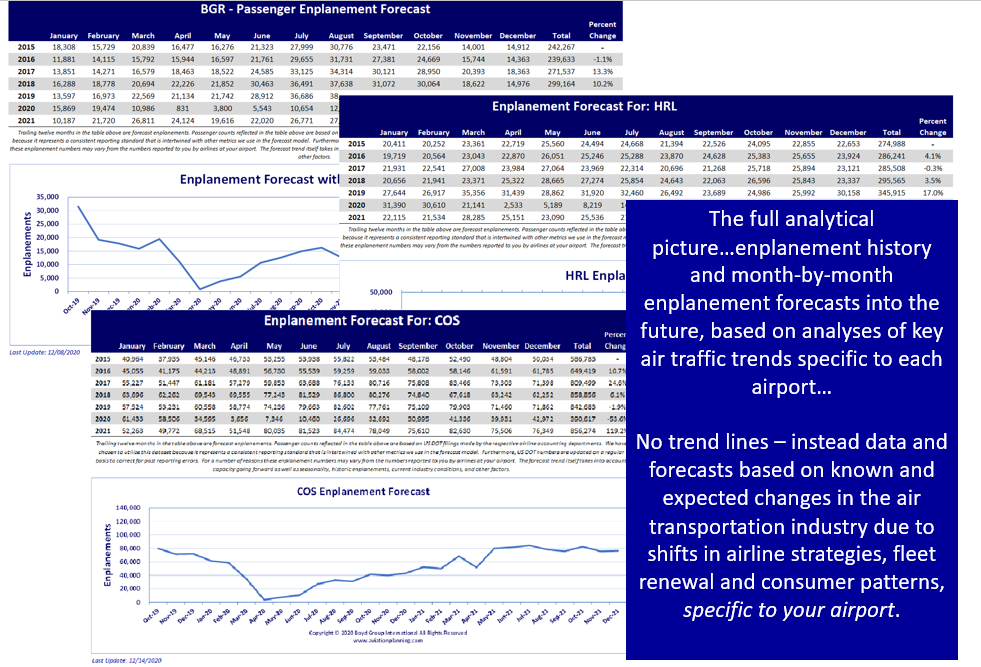

Airport-Specific Short-Term Forecasts Available

Question: What is the message based on the expected changes in enplanements in January, as noted above?

Answer: it is now airline corporate decisions, not necessarily local and regional economic factors, that are the prime drivers in the volumes of passengers that airports can expect. Airlines are in restructuring mode, and they put a lot less – if any – reliance on traditional “market studies” fed to them from the outside. The last thing they want is a wandering 40-page study chock full of fun graphs and heat maps that have no bearing on the strategic direction of the airline itself in the current survival environment.

This is a whole new economic and operational situation for airports – one not experienced before. Long-term planning cannot be accomplished without a firm grasp of the near term, and that “near term” is going to be the product of airline strategies as they re-order fleets, staff, hub spokes, competitive position and other factors.

Today, the entire short-term forecast picture – from airlines, to suppliers, to consumers, to facility needs – has completely changed. As pointed out in the above filing, the underpinnings of the airport business can and will change in a flash.

This is the reason that BGI is making available Airports:USA Short Term Forecasts, covering the specific dynamics expected in the next rolling 12 months.

For the immediate future, enplanements will be primarily the outcome of factors outside the traditional realm of local and regional air service demand. Instead, it is the airline industry that will make the fundamental changes that will determine traffic levels. It’s here where Boyd Group International’s Airports:USA system can deliver new perspectives and new planning vision.

For more information on how to subscribe, just click here.

Don’t plan in the dark. And more importantly, don’t plan on the basis of pre-China virus assumptions and metrics.

We look forward to working with you!

_______________