One More U.S. Victim of the CCP’s Corona Virus

Another Reason for Airports to Pursue Recompense – But There Will Be Push-back From Unexpected Corners

The CPP-COVID virus may be slowing its expansion, but the financial damage continues to spread.

Here’s another example – a small footnote in the newspapers, but another indication of the range of the damage this pandemic continues to inflict on the lives of thousands of people.

The Commonwealth of the Northern Mariana Islands is facing a revenue crisis, big time.

The cessation of tourist flights from China to Saipan has hit the airport system with a nearly 50% cut in total revenues. Not inconsequential, and the immediate proximate cause is the CCP-COVID pandemic, and secondarily, the emerging and continuing political thuggery of the CCP toward the Chinese people, plus a concerted program to convince the Chinese public that the USA is responsible for the emerging economic plunge starting to manifest across their country.

The CNMI government has petitioned the DOT to exempt them from the restriction on flights from China and Hong Kong, noting that this traffic is critical to the Commonwealth’s economy.

Here’s some troubling news for our friends at Saipan and the region: with or without allowance of additional frequencies, this traffic segment – Chinese tourists – is toast. They aren’t coming back.

The reality is that the Chinese Communist Party has been working very hard to vilify the United States and convince Chinese citizens that it would be unpatriotic to travel to the USA. That includes Saipan and Guam, just like Harrisburg, Moab and Las Vegas.

Point: the CNMI, as well as other formerly-favored destinations on the part of Chinese visitors, need to find other revenue sources. This one is kaput.

A Complete Change in Just 36 Months. We would point out that this is a complete 180 from the situation just three years ago.

Back then, before the Xi Jinping clique fully put the dogma screws to the Chinese public, the market appeared to be almost unlimited. BGI was at the forefront of this, with our ChinaNiHao team. We were working on both sides of the Pacific to make China-U.S. travel continue to expand.

Not anymore. The China-U.S. leisure market is gone. President Xi and his sinister team of un-elected government hoodlums have seen to that.

For those interested in updates on the China-US aviation situation, bookmark www.BoydGroupChina.com. We’re developing the site into an independent source on China, including the criminal culpability of the Chinese government in the COVID-19 pandemic.

Second-Agenda Media Protectors – Don’t Expect Hard Facts. Keep in mind that some American news sources have a lot of dogs in the fight and money invested in China offices, not to mention associates there that can be subject to “discussions” with CCP authorities, should an article appear that they don’t agree with.

So, in a very real sense, a lot of these entities are defenders of the CCP in the USA, whether they intend so or not. They are part of a de facto fifth column that Beijing can depend on to cloud the facts.

Let’s not dance around the politically-correct maypole. A few of these supposedly unbiased media channels will at the least have the tendency to sugarcoat the stories, leaving out facts and points that are unfavorable to the CCP. Or, more blatantly, like 60 Minutes, righteously mislead the public, implying that it’s disinformation to blame the Wuhan Virology facility for the virus. Not true.

Let’s not dance around the politically-correct maypole. A few of these supposedly unbiased media channels will at the least have the tendency to sugarcoat the stories, leaving out facts and points that are unfavorable to the CCP. Or, more blatantly, like 60 Minutes, righteously mislead the public, implying that it’s disinformation to blame the Wuhan Virology facility for the virus. Not true.

In March, one major American financial journal published an article covering how various global regions were responding to the pandemic. The online edition included a video purporting to explain how the virus spread in the first place. It completely sidestepped any real facts on what happened in Wuhan. It simply noted that the Wuhan authorities had discovered the contagious nature of the virus, and then the video skipped to telling the readers that an infected person was then found in Thailand, and then others elsewhere in Asia. This was their story on how the spread of the disease got started.

The financial journal’s video completely left out the events and actions in Wuhan and in China that were the direct causes of the spread. Not inconsequential. In light of what was clearly known at the time, it was a whitewash, or else the product of really amateur journalism.

No mention was made of the cover-up and direct misinformation to the citizens of Wuhan, who they encouraged to participate in enormous communal New Year feasts and other events, right up to 48 hours before they gave up the ruse and declared the epidemic. The reporters for the august financial journal didn’t mention the efforts by the CCP Wuhan government to convince residents that the virus was not transmittable, including videos of happy citizens dancing around without masks, singing “bu pa!” – not afraid. The respected journal made no mention of the muzzling of medical staff to not report the danger.

The respected financial journal didn’t focus on how, even when knowing the contagious nature of the virus, the CCP allowed millions to travel from Wuhan for the New Year festival to points all around China and the globe. They just pretty much jumped to the infected guy discovered in Thailand.

It’s like reporting on how the U.S. got into WWII and skipping the part about Pearl Harbor.

At best, sloppy journalism. And even that is a hard one to swallow. In any case, it shamefully misled and misinformed the public. It served to protect the CCP from any hint of the massive and criminal malfeasance they engaged in. We did e-mail the writer of the article, noting several facts missed in the video. Naturally, the people who put it together never responded.

Thinly-Veiled Paid Advertising For The CCP, Postured To Look Like Reliable Facts. Not only that, but, incredibly, in the past week it has come to light that several U.S. media channels have accepted payments – some in the millions – in exchange for printing “advertisements” that although have “advertisement” on the header, still look a lot like articles, provided by the China Daily. It’s a newspaper run by the propaganda department of the Chinese Communist Party. Over the last four years, they’ve paid at least one major U.S. financial journal $6 million dollars to place these “ads.” Therefore, they are a customer of the media channels they do business with.

The question comes up whether in stories done covering China, this business relationship – the CCP being a more than million dollar annual (on average) advertiser – should be disclosed. Furthermore, due to the clear nature of the CCP, and its repressive nature toward free speech and human rights, it might be suggested that the propaganda nature of the inserts should be clearly illuminated, and not just routinely placed, along with ads for watches or automobiles or expensive clothing.

These and the invested interests still doing business in China are financial dragons that a lot of people on this side of the Pacific do not want to get gored.

Another issue of caveat reader.

How Badly Has Your Airport Been Hit? A final point. The CNMI is not alone. Airports across the USA – from ALB to YUM – have suffered enormous financial losses, specifically and directly due to the CCP. Hundreds of millions.

At some point, Congress will implement mechanisms that can be pursued to demand recompense. It’s not about suing a foreign country. Remember, just about all Chinese investments in the U.S. are actually connected to the Chinese Communist Party. They run China, but they themselves are not a sovereign nation. Theoretically, then, there’s close to $150 billion in CCP assets in the USA.

Now, we are talking about federal channels that may be developing. This is not a matter for the late nite TV ads with law firms trolling to find clients to participate in semi-ethical class action suits that will line the lawyers’ pockets first and leave victims with peanuts. This situation is not like a defective weed killer or an obscure acne medicine that caused peoples faces to fall off. This is a nationwide matter that has affected all citizens, and it’s well beyond the scope of legal firms trolling for quick business. It will be the feds that run the show.

Boyd Group International is ready to assist airports and communities in developing accurate, supportable and professional projections of damage done directly by the CCP-COVID pandemic. There are direct revenue losses. There are job and economic losses. There are market opportunity damages as a direct result of the CCP-pandemic. The key is to have a clear set of defendable projections.

We can help. Having this information now will be a benefit when (not if) the federal government takes action to hold the CCP accountable. Remember, anything that threatens the CCP will bring on the the type of nonsense journalism described above. Hard and unshakable data is the only protection.

Make no mistake, at some point in the near future, it will be time to drag the CCP dragon into court.

____________

Rebound Check

It’s real.

Traffic demand is returning along with the rebound in the economy.

First, consumer sentiment is pushing well into the “let’s take a trip” mode. Second, the airline industry is clearly seeing this and pulling more aircraft out of storage.

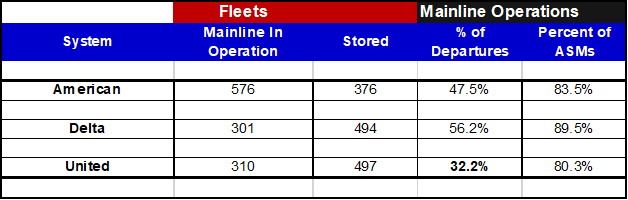

This is all great news. But there is a lot more capacity and demand that will be put into the system in the next six months. Here is a snapshot of active v stored mainline aircraft at AA/DL/UA, along with the percentage of departures and ASMs that are scheduled to be operated in-house in July, as opposed to use of fleets of contract carriers (the mis-named “regional airlines” which are essentially in the business of leasing aircraft operations).

Without getting too deep into the numbers – which are changing daily – it’s clear that the three systems have different rebound and fleet strategies. (Note that the Delta data for stored aircraft do not include recently retired fleets of MD-88, MD-90, and soon to go B717s.)

New Air Service Access Dynamics – A New Playbook

However, we will need in the future to recognize three key emerging dynamics within the post-CCP-COVID air transportation world.

Airlines have taken, and are continuing to take, a financial hammering. The fact is that the financial underpinnings of the U.S. airline system will be very different. Carrier systems have had to bring in a lot of new debt. This means that route and market planning will be different.

That $1 million SCASD grant in 2021 likely won’t be enough to get them to answer the phone – assuming the skeleton planning staff has time to even pick up the receiver. It means the curtain of reality will be continually pulled open at some smaller airports, revealing Oz-like nonsense being peddled on them to “find more airlines” when there aren’t any to start with.

Consolidation of route systems will be very apparent. We are going to experience more regionalization of access – particularly hitting smaller airports and metro-peripheral airports.

Airlines will not be as interested in wallowing through more “true market studies” that belabor a whole lot of data that are inconsequential to the fleet and strategic realities of the new air transportation system. As for “leakage” studies, the answer will increasingly be, “Yup, know that. And we’re after more. We’re focused on continuing to regionalize access. Thanks for sharing.”

New fleets will emerge – with new mission envelopes. With the accelerated retirements of parts of airlines’ fleet mix, the replacements will focus on new multi-mission-capable narrow-body airliners such as the A220-300 and the A321XLR. Stand by for more foreign invasion of interior U.S. airports.

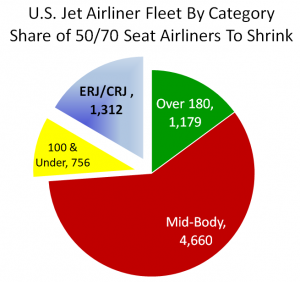

Along with this, the capacity floor at major carrier systems will gravitate to 76-seats and above. Plan on seeing fleets of 50-70 seat jets pulled out in the next 24 months.

The key to developing the new-future air service access program will be in understanding airline fleet plans.

The markets will adjust to these, not the other way around.

Re-Planning The Future. For airports now reassessing their air access development plans, Boyd Group International stands out. Our focus is on identifying emerging trends in fleet mix, expansion strategies, and consumer preferences that have been affected by the shutdown of the system due to the CCP pandemic. Past traffic and demand data are now only fractionally valuable in the planning process, because the industry is rebounding with different financial dynamics.

To get a fresh view of the future, give us a call or a quick e-mail and we can discuss .

_________________

The International Aviation Forecast Summit Is On!

This will be the first post-CCP-Pandemic event that will cover the future the industry faces.

We will not rehashing what’s happened, but looking at how we can optimize coming out of the economic wreckage foisted on the air transportation system.

We will not rehashing what’s happened, but looking at how we can optimize coming out of the economic wreckage foisted on the air transportation system.

Clear your calendar for August 23-25 and join aviation leaders in Cincinnati, USA to get a jump on the future. Click on the icon to register.

_________________

ALL OF US AT BOYD GROUP INTERNATIONAL WISH YOU A PROSPEROUS AND HEALTHY WEEK AHEAD!