Before We Get Started This Week…

Taking Flight Symposium – Regional Air Service & Beyond

Boyd Group International was invited to take part in the Taking Flight event held by the Washington Post In New York City, October 7. As a major aviation research and forecast firm, the Post was interested in our perspectives on a range of emerging air travel dynamics.

The event included discussion sessions regarding the challenges facing air transportation and logistics. New technologies in communication and in consumer options were front and center at the event.

Sponsored by Mitsubishi Heavy Industries, which now has a re-designed 100 seat airliner under development, the focus was on how air travel – and travel in general – will evolve in the next decade.

Sponsored by Mitsubishi Heavy Industries, which now has a re-designed 100 seat airliner under development, the focus was on how air travel – and travel in general – will evolve in the next decade.

On the session specific to regional air access, Mike Boyd and former FAA Administrator Michael Huerta candidly took on very incisive questions from Washington Post transportation reporter Libby Casey.

Hot button issues, such as trendy suggestions to “shame” people from flying due to alleged harm to the environment, the concept of “high speed” rail, airport congestion and the pilot situation, were tackled directly and concisely.

Also on the agenda were Robin Hayes of JetBlue and Blake Scholl of Boom Technologies, which is well along with a 65-70 seat supersonic airliner.

According to numbers from the Post, over 150 people attended, and the live podcast attracted 45,000 visitors.

Boyd Group International is honored to have been included at this high-profile event.

_________

This Week’s Insight…

The China Opportunity –

It’s All About Economic & Political Evolution…

And A Clear View of The Future

Lots of smoke. Lots of mirrors. And a whole lot of economic gravity about to assert itself.

That latter part about gravity might soon resemble the economic equivalent of a baby grand getting tossed out of the eighth floor window.

We are talking about the near-term evolution of business and air travel demand between the China and the US.

A Temporary Mirage – Or Part of A Developing Economic Roller-Coaster?. Just three years ago, the China-US picture was looking about as rosy as one could imagine.

Foreign direct investment – FDI – from China was booming – reaching nearly $50 billion annually. EB5 programs were in vogue, bringing more Chinese investment into projects across the US.

General Electric sold its white goods appliance business to Haier, in the pattern of IBM selling its computer and server businesses to Lenovo. Things like new Chinese-owned tire factories in rural North Carolina were regular news. Economic cooperation was in full swing.

And back in China, things were just marvy, too. Forty years after economic liberalization, China is developing a middle class that in many ways is a dead-ringer for the USA. Television shows in China typically showcase happy families in comfortable American-style homes and apartments, commuting to clean white-collar 9-to-5 jobs in their Buicks or Toyotas or Volkswagens, living a life that isn’t too far off what Americans see in shows like “Friends” or “Seinfeld” or (has this gone too far?) “Leave It To Beaver.” One popular Chinese TV sitcom actually includes a character who has a late-night call-in radio show…open and free discussion, when he’s not meeting friends at sleek cocktail bars.

It’s Not Your Father’s Red China, Anymore. It’s on a totally different planet from the 50s, 60s and 70s, with blood-thirsty mobs chanting slogans, marching to support a defined-for-the-next-ten-minutes “cultural revolution,” aimed at ferreting out evil bourgeoisie running dogs of capitalism, and sending families wholesale to reeducation camps. At least the traffic in Beijing was less congested. There wasn’t any.

In the 1970s, folks leaving mainland China were escaping, not traveling on return tickets. Today, air travel has been delivering huge movements of Chinese consumers eager to see the USA. Growing every year, finally reaching over 3 million by 2017. Chinese visitors are increasingly common across the USA. Accommodating them and their $6,000 per-visitor spend, has been big business at venues all across the USA. Amid soaring if geographically-uneven economic expansion, China is – or now, was – on track to be a huge consumer powerhouse.

Cracks In The Foundation – But Repairable. Alas, this new economic model is now in line for some heavy re-structuring. Along with the economic boom, a correction – or set of economic corrections is in motion.

This is important for air service planners to understand when crafting programs for China access – including at communities that will be accessing the Middle Kingdom via connecting itineraries.  The rapid expansion in air service access will slow temporarily, but they need not be misled into believing it’s over. Planning for 2023 and what will be a huge flow of new business and travel demand from China is still imperative.

The rapid expansion in air service access will slow temporarily, but they need not be misled into believing it’s over. Planning for 2023 and what will be a huge flow of new business and travel demand from China is still imperative.

It just won’t look much like we’ve seen in the last five years.

For the moment: a lot of the economic expansion seen in China is not fully founded on solid reality. For the next 12-18 months, there will be significant corrections in economic growth directions in China as they affect air access to and from points in the USA.

In the last 12 months, FDI from China has almost completely evaporated. For the first time, Chinese visitors to the US dropped in the first quarter of 2019 – by six percent, and Boyd Group International forecasts indicate a decline of more like 12% by the middle of 2020.

It’s The Economy, Ben-dan… The Chinese Economy. Okay, we will start with the hard news… the China-US air travel picture will be a lot more sugglish near term (12-18 months) than now being assumed. There are major issues – all relevant to events in China – that are in play.

As for the decline in FDI, the market has changed. Both the capital available in China and the low-hanging targets to buy in the US have largely been picked clean. Over-investment on the part of Chinese conglomerates like HNA and Anbang has led to their shedding of many former investments in America. It’s not politics in this case – it’s a need for a market correction.

In China, a lot of the discretionary money generated by the real estate boom in major cities is starting to evaporate. Auto sales in China are down a whopping 15% – a sure red flag that discretionary income is slipping big time… that’s the same income sector that drives Chinese tourists to Yellowstone, Niagra Falls, and Chocolate World.

Huge Chinese real estate projects – many generated by municipalities playing fast and loose with investment laws – are coming up croppers. There are literally entire cities that have been built on spec and are empty. Financially, a lot of investors are getting schnookered. Banks are getting shaky. One relatively small bank in northern China reportedly needed a $90+ billion bailout earlier this year.

Then, there is a massively slowing economy – officially it may be below 7% this year, and actually may be a lot lower. There are factories that are closing and the fact is that, socialist doggerel aside, there isn’t much in the way of a social safety net in China. Also, China is finding that a lot of what they export can also be made elsewhere in the world, cheaper and with less bureaucratic hassle. Then comes robotization of factories – which erases much of China’s labor cost advantages.

Oh, and the politicians and some in the travel industry on this side of the Pacific who can’t control themselves from blaming this on “Trump’s trade war” – they’d be well advised to get some facts, first. Actually the fallout of the U.S. “trade war” on China is the equivalent of whacking a small dent in the fender of a pick-up truck that’s already been t-boned at a railroad crossing.

Oh, and the politicians and some in the travel industry on this side of the Pacific who can’t control themselves from blaming this on “Trump’s trade war” – they’d be well advised to get some facts, first. Actually the fallout of the U.S. “trade war” on China is the equivalent of whacking a small dent in the fender of a pick-up truck that’s already been t-boned at a railroad crossing.

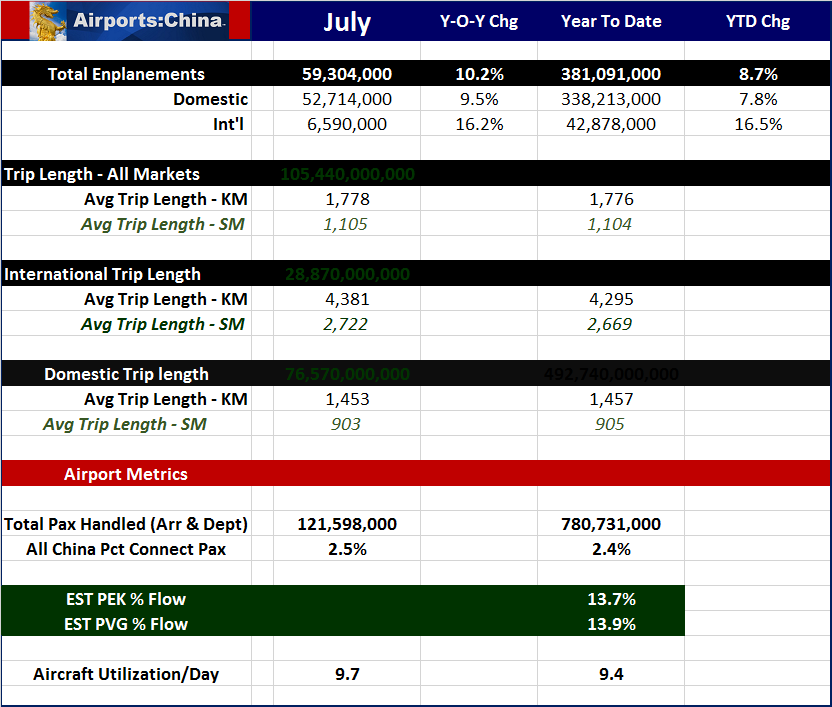

So, Where From Here?. Economic corrections tend to be positive processes. There is a huge sea-change coming in the basic foundation of the Chinese economy. Our Airports:China forecasts are based on the actual growth generating at most an annual 5.5% increase in air traffic in China over the next five years.

But what we’re going to be seeing emerging in the next 12-18 months in regard to China-US travel and investments will be fundamentally different and a whole lot stronger long-term (36-60 months) than expected. Lots of structural changes. Take it to the bank… by 2023, China-US air travel demand will skyrocket. To be sure, a lot fewer tour buses descending on US shopping malls, disgorging Chinese intent on buying a Louis Vitton clutch. But more business and FIT travel.

Even Montana May Benefit. Example: Yellowstone will likely see a decline in Chinese tour movements, and a decline in total visitors from China. But it will see an increase in individual travelers … the category that tends to make flight connections to interior points, rents a car, and sets its own itinerary. That means that as a result, airports such a Bozeman will be seeing an increase in Chinese travelers. Not enough to build a new rental lot, but another 2,500 – 3,000 annual passengers that weren’t there in the past.

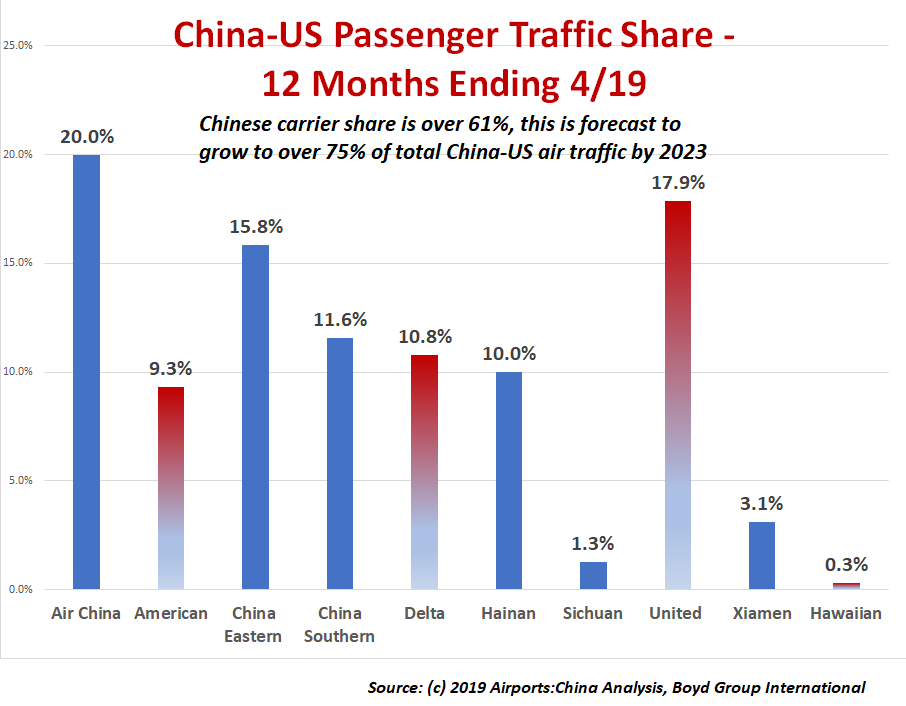

Another key point is that it will be Chinese airlines that will be the major players – either to their US alliance partner’s hubs, or via one of the emerging independent Chinese carriers. As the graph indicates, today traffic on US airlines metal is less than 40% of the total… and as the market even grows, that share will still decline to less than 25% by roughly 2025.

But it’s still a growing pie. Today, due to the structure of China’s air service system, our forecasts indicate that less than 12% of the total potential demand for China-US travel is being met. Without true connecting hubs, and actual restrictions in airline-to-airline interlining, that natural demand is simply cut off.

But along with the economic re-structuring, China’s air transportation system is also changing. Interlining is being implemented at the 29 largest Chinese airports, which today account for more than half of all passenger generation. There will be two US-style airline connecting hubs at the new Beijing Daxing airport, another at Beijing Capital, and a fourth at now-expanded Shanghai Pudong.

Put this together – a growing economy based more on realities that unbridled optimism, and four giant airline connecting hubs, and this is the green light for every US hubsite airport, and it’s full speed ahead in planning for for every US secondary airport that is in a geographic centroid of Chineses business and educational investment.

Point: strategic planning demands looking over the horizon. It requires having a clear vision of future dynamics. It often requires the need to put “ambient” thinking and trend-lined data aside and make independent determinations of the future.

__________________________________.