March 22 Insight To Be Posted Shortly!

The Traffic Picture – U.S. Positive. International Not So

The Main Concern – Changing Policies From The Economic Hobbyists In Washington

We can start with this: the U.S. airline industry is in better shape than any other in the world. One reason is that, aside from China, it is the only one that’s based on a huge domestic demand.

A recovery is starting to show… the capacity knife was used a lot less on the originally-filed schedules for March… as it stands, it appears that this may be the case with April and beyond.

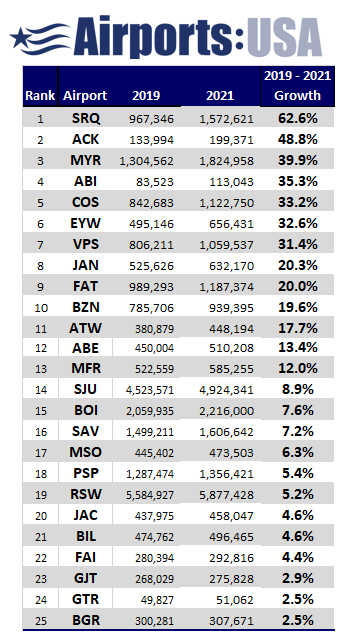

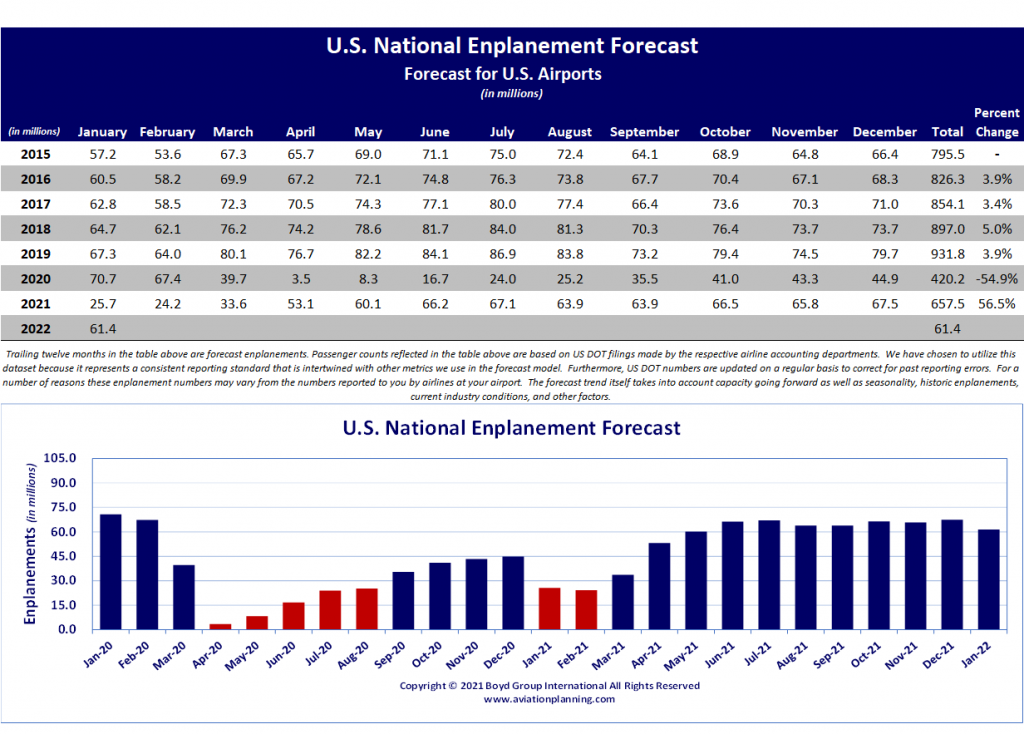

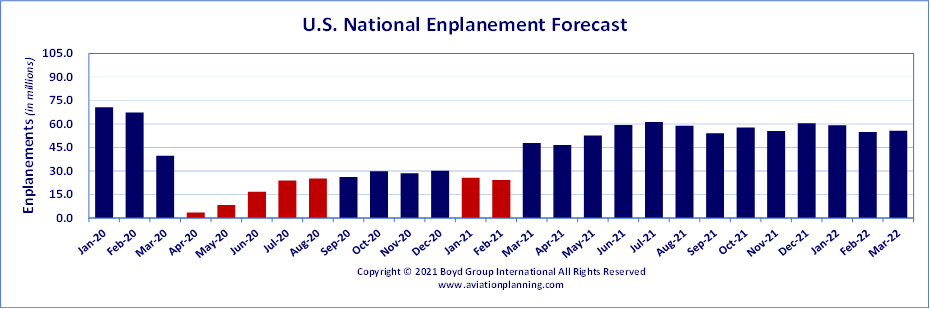

The latest Airports:USA® short term forecast:

If the trend holds, if the economy holds, if new taxes are not imposed, if the increasing constriction on petro-production on the part of the inhabitants in Washington doesn’t jack the price of jet-A up, the traffic recovery will be quicker than estimated three months. A lot of ifs.

The Welcome Signs Are Coming Up. A number of states have made the decision to completely or almost completely open up. The requirements to cover one’s nose and mouth – regardless with what (N95 or a used hankie are both regulatory-satisfactory), and regardless of where one is, or how effective it may be – are being lifted in several states.

This removes the barrier and uncertainty of traveling to major places such as Texas and Florida. Other states are still in a state of CCP-Covid confusion. Nevertheless, the picture is clearing.

That’s in the United States. Not so in the E.U. or the U.K. Latest news is that Italy may shut down, and it appears that guy with the run-away hairdo who’s running Merry Olde England is clueless. Canada is still constricted. Same with other parts of the globe.

A New U.S. Air Transportation System. New Airline Strategies. Amid all this, the restructuring of the U.S. air transportation system will continue. The main apparent trends are:

- Expansion of Leisure Destinations… Florida is the main recipient, but any flows that can be identified as having potential leisure stimulation are in play. Montana is another opportunity. The goal is to plumb into some of the money not spent over the last year.

- Major City – Secondary City O&D Market Spokes. Big markets such as Los Angeles can offer potential of stimulating day-of-week or low frequency service to mid-size airports that in pre-CCP-Covid days weren’t really opportunities. In regard to Los Angeles – and California in general – it will all depend on some regulatory consistency coming into the picture.

- Expansion of Hub Flows. American in particular is bulking up on accessing secondary airport flows, particularly at CLT. Great news for some regions… how fleet changes will affect this in the long term is uncertain.

The U.S. airline industry went into full metal jacket mode almost immediately upon the arrival of this gift from the CCP in Wuhan. It’s clear that every airline now has an aggressive and internally-generated strategy to deal with the effects of the pandemic and the sometimes herkie-jerk responses on the part of some state governors.

Meantime, Back In The Old Countries… The situation in the rest of the world is not encouraging. As noted above, Europe is completely in planning chaos. Australia is still restricted in regard to international access.

Asia is not only affected by the CCP virus, but by widespread and very uncertain political issues, mostly driven by the 21st century Nazis running China. (The chief Don of this criminal enterprise has instructed his army to prepare for war. It may be more than the usual doggerel, based on infighting between factions in China. Think Kinmen or even Taiwan as “points of interest” in the next 12 months.)

The point is this… the main reason for the plunge in domestic air traffic in the USA was first fear of the disease, and then the uncertainty of whether entire cities might be shut down. Both of those factors are receding. Domestic traffic levels will rebound faster than recently forecasted.

But the emerging national and global air transportation systems are still structured for the world of 2019. That’s dead… the roles and utility of air travel have been shifted. Leisure, business and international travel patterns have changed and that means airlines are facing new fleet imperatives.

As noted last week, the era of the “regional jet” – defined as 70-seats and below – is over. The next big trend will be in the single aisle category, with A320neo, 737 MAX and A220 variants opening secondary airports to a much wider set of new market opportunities.

Danger Signs… Torpedoes Spotted. The only uncertainty is how the economic plans being ginned up by the inhabitants of the Marble Play Pen will slow all this down.

The indicators are not positive. Standby.

__________

In The Latest Aviation Unscripted Video…

The Realities of Establishing Air Service At Small Communities…

Time To Stop The Games

Getting scheduled flights into small unserved airports has been one of the most misunderstood – and abused – challenges in the realm of air service development schemes.

Getting scheduled flights into small unserved airports has been one of the most misunderstood – and abused – challenges in the realm of air service development schemes.

The problem is that there is the belief that unless a community has scheduled flights at the local airport, the economic future for that community is dead. In most cases that is pure hogwash, and in any case often completely impossible.

What these ASD programs usually ignore is the consumer… civic hubris and another jive-time “Market Study” won’t replace superior air service options.

We grab this third rail in the current Unscripted video,,, click here to join us as we explore reality.

_______________________