Monday, January 19, 2025

Why Frontier & Spirit Won’t Survive

They’re Playing To An Audience That’s Left The Building

|

|

|

|

|

|

Monday, January 1, 2026

Allegiant/Sun Country Merger Works.

Also Proving Why Frontier/Spirit Would Be A Disaster

Lots of coverage of the acquisition of Sun Country by Allegiant. The usual suspects in the shallow end of the analytical pool are starting the usual doggerel.

One of the usual gadflies already has declared it a takeover of “a rival” by Allegiant. That’s true only to the extent that much of SY’s model is to go after discretionary impulse leisure traffic, as is the MO with Allegiant. But as for direct route competition, not much there.

One of the usual gadflies already has declared it a takeover of “a rival” by Allegiant. That’s true only to the extent that much of SY’s model is to go after discretionary impulse leisure traffic, as is the MO with Allegiant. But as for direct route competition, not much there.

One of the reasons for a merger is to combine strengths, financially if not route system wise. Another is to deliver a stronger entity for shareholders, employees, and the target customers.

This deal satisfies all these requirements.

Fleet Planning: Solid & No Financial Sleight-of-Hand. Take a look at Sun Country. They have about 47 Boeing 737s in passenger operations, plus 20 or so placed with Amazon, and as for the backlog of additional airliners – there are roughly two – count them, two – 737-900s. That for now is it. Not a lot of risky nonsense about add-planes-and-we-gotta-expand.

As for Allegiant, they’re at around 121 airliners. Today, that includes 16 newly arrived 737-8s. But it has another 100+ MAX 737s on order, which likely would mostly go toward replacing the 84 remaining A319/320CEOs in the fleet, which means Allegiant is in the air travel business, not the sale and lease-back business as is Frontier.

Two solid operations. No real overlap. No hidden imperatives for the merger to address. No reduction in consumer options – mainly because these are airlines with a model that offers the product first, and by doing so attracts passengers.

A Solid Leisure Niche At MSP. For Delta at MSP, this deal should not immediately trigger any heartburn. The SY/G4 combination is something they will watch, but for the foreseeable future, there is slightly less than zero chance that Allegiant will be a direct product threat. Yes, they will compete for consumer impulse leisure decisions, as they do today at MSP, but the product variance is real. Demonstrably real.

Taking a look at Sun Country’s focus on MSP, it’s clear that the differentiation in consumer targets is working. For the YE 9/25, according to our friends at Airline Data, Inc., Sun Country achieved 3.6 million MSP passengers, at an 83% load factor. The largest key markets – MCO, PHX, RSW, LAX, etc. – tended to be closer to 90%.

What we have here is a pretty clear separation of market products at MSP. Much of the traffic sitting on SY airplanes at MSP probably were not taken from Delta. They were created by Sun Country.

It is going to be of interest to now see what’s probably going to be a flood of media suppositions about this deal prodding a Frontier/Spirit merger.

Not a pretty picture. Spirit is scrambling to find a new route system, and is parking airplanes and having operations problems, both internal and due to the RTX engine issues. Frontier has a losing strategy of sprinkling a couple flights here and a couple of frequencies there across the country with reliance only on a low fare to showcase the service. It lost $190 million through September.

Plus, as respected analysts such as Jamie Baker have pointed out, F9 is relying on new aircraft deliveries to fund sale-lease back transactions that are keeping much of Frontier afloat. Lots of 240-seat A321 behemoths.

Point: The Allegiant acquisition of Sun Country is based on solid strategy and two well-managed airlines. A Frontier/Spirit merger would combine a whole passel of weaknesses and fundamental planning mistakes and solve none of them.

Bluntly, it would be the financial equivalent of a mid-air.

_________

Monday, Jauary 5, 2026

Air Service Regionalization & The Flat Earth Society

Children’s Crusade: Bring Back Small Airport Flights

Another hard truth that will come into play in 2026 will be the end of the scam surrounding small airport air service. The truth can only be ignored for so long.

Another hard truth that will come into play in 2026 will be the end of the scam surrounding small airport air service. The truth can only be ignored for so long.

Here’s some really bad bedside manners for the folks lamenting the “loss” of air service (undefined) at small airports. Wake up and join us here in reality. If only as a temporary tourist. That air transportation system – operated by independent “regional airlines” is dead. Let it go. No CPR necessary. It is gone, and new economics are in place.

Secretary Duffy: Please Clean Out That DOT Mushroom Garden. A couple weeks ago, a really inept study was issued by the Department of Transportation, lamenting how non hub airports are continually losing scheduled passenger air service. The conclusion was that small communities are being cut off from the national economy.

No air service at the local airport simply means economic decline, the report concludes. ‘Course, the DOT does not define “air service” in any qualitative manner. Just flights.

Nevertheless, this study was very valuable. Valuable in that it completely demonstrated how off-reality and obsolete are a lot of the wasted efforts to keep transportation planning firmly rooted in the 1950s.

The concept of relative quality of air service access was not in evidence in this study, nor typically in the oft-published lamentations of the passing of independent “regional airlines.” Too advanced in thinking for these people. They want “regional airlines” back.

Luddite is one word to describe it. Ignorant is another. Shamefully sloppy and misleading is yet another.

The folks pushing this stuff ignore the basic foundations of air service – which is time and convenience, not local flights. They have no concept about consumer value. They are misleading the public into believing that “air service” is just about the local airport, and not about time-efficient communication and consumer value.

The mantra is dismal. Gotta have those glory days of “regional airlines” come back. Even though that entire sector – independent regional airlines – atrophied and went glub-glub over thirty years ago. For economic and consumer reasons.

The mantra is dismal. Gotta have those glory days of “regional airlines” come back. Even though that entire sector – independent regional airlines – atrophied and went glub-glub over thirty years ago. For economic and consumer reasons.

Desperate Studies To Re-create Yesterday. There was a coffee klatch study on small airports done by the Transportation Research Board. Published in 2017, it even concluded that congress should fund development of new small airliners so that small communities could see the return of the glory days of skies blackened by C-402s, B-99s, C-212s, S-340s, M-IIIs and the like.

Waiter! Check please!

The economics involved and the core dynamics of air transportation took a distant back seat to pandering veneer civic boosterism. It was a total waste of money, because it assumed that airports and not communities and regions are the focus.

Air Access – Not Local Air Service. The fact is that today, consumers in small and rural communities where the local airports no longer have scheduled flights, are by and large facing far better air access than when those small airliners were operating.

Yes. Better.

The core tenet in most of these Walter Mitty small airport studies is that having to drive to an airport other than the local one is a torpedo to the future of the community. Then we have the perfunctory “leakage studies” that mislead the public that geographic factors alone determine potential airport traffic, in total absence of any analyses of alternative consumer options.

Maine: Economic Hardship, According To The DOT. Let’s look at the disaster that we’ve seen in Maine over the last several decades. A disaster at least within the amateur-act rationale of the folks at the DOT and lots of gadflies in the media.

In the early 1980s, Waterville, Augusta and Lewiston, all in central Maine, had scheduled passenger air service. Operated by a small commuter airline, with typically multi-stop limited frequency to Boston.

The alternative for these communities back then was a short drive (an hour or so or less) to Portland. Not a lot of incentive. At that time, PWM was only served by Delta Air Lines and a small commuter. Air Vermont was in town briefly with flights to Burlington, until the FAA got wind of its sloppy maintenance.

As for flights out of Portland, not much happening, back then. Delta basically flew to Boston and maybe a flight to LGA. The commuter also served Logan, along with a multi-stop occasional schedule to Hartford/Springfield and ultimately to New York. At one time they tried nonstops to Philadelphia, but that pretty much was it.

Fast forward to today. Those abused and isolated consumers in Augusta and Waterville and Lewiston now are forced into that brief drive to Portland – an economic death sentence, according to the DOT and consumer wags longing for the good old days of “regional airlines.”

And today at PWM, the consumer, no doubt wearied from the 60 minutes or less on I-95, no longer has the convenience of choosing between just two airlines. Now, there are six jet airlines, serving twenty nonstop destinations, including seven major airline connecting hubs. American is there with flights to DCA and CLT. Southwest, too. Breeze is doing nonstops to Florida. JetBlue has flights, too.

Anybody see the realities here? The Maine Scenario – where regional consumers have much better, wider and more efficient air access than can ever be supported at those supposedly doomed small local airports – is typical across the USA. Even at larger cities.

One poster child is Toledo, which has excellent air service. But it’s not at the immediately local airport, anymore. It’s a 60 minute or so drive to access the over 300 nonstops daily at Detroit Metro.

All the King’s consultants and all the King’s jive studies notwithstanding, it would be really a challenge for TOL to support any local network connective air service that can compete in terms of total travel time and convenience.

In any case, this is the future of air service across the USA. Britt Airways and Wings West and Precision and Rio and the rest of the 1980s regional carrier rogue’s gallery are not coming back. As clearly demonstrated in repeated in-depth analyses by Swelbar-Zhong, air travel is now truly multi-modal due to an excellent highway system.

This is the reality, no matter what the DOT puts out. No matter what civic hubris can generate. Resistance is futile.

And anti-consumer, too.

The next dynamic to watch will be a temporary spike in availability of 50-seat lift at SkyWest, with some branded small airport flights coming online. Don’t get too excited, the economic writing is in the sky.

The next 12 months will be a watershed in rural air service.

_________

Monday December 23, 2025

A 2026 Aviation Tickler

A Few Random Observations Outside The Consensus Orbit.

Southwest: Product-wise and consumer strategy-wise, has it completely crossed the Rubicon? Or is the competitive current taking it downstream?

The Collapsed ULCC Sector. Not a reduction in competition as much as elimination of a consumer leisure-spend option, as well as capacity that has been based on operational cost factors that no longer exist. Survivors have circled the wagons in new strategies.

Is Embraer Poised For A Comeback? The ERJ-195 E-2 now has a 100-plane deal (orders and options) from a US carrier – Avelo. This might spur more global interest v the A220.

The Las Vegas Product Shift. The supposed jump in LAS visitor costs will tend to affect small airports where day-of-week impulse flights are a high percentage of enplanements. What happens in ‘Vegas affects Stockton.

The Lift Contractor Segment (a/k/a “Regional Airlines): A lot of contract extensions, but how many will be doing flying that’s vulnerable to being brought back in-house? Is Air Wisconsin more than a one-off? Is Mesa/Republic a harbinger?

New Tech Starting To Leapfrog Airbus/Boeing/Embraer? Boom Supersonic ignored the consensus. Now another company is claiming to have a whole new blended wing aircraft under development. Is there something here regarding how airliners are developed?

Small Community & Rural Air Service. The paucity of airline players is tending to make speed date conferences less valuable. Any community that needs to go to one of these events to find and “lure” unidentified airlines is wasting time.

CRJ200s: A Near Term Bubble. Availability of excess 50-seaters could bring some increases to a few small communities. Pro-Tem only.

Customer Product Is The New Battleground. United and Delta are demonstrating that leveraging customer contact programs is a competitive advantage.

More EU Carriere Invading Trans-Atlantic. Consider the Aer Lingus experience – feeding their Dublin hub with US market entry. Might LOT or SAS or EU carriers chase that USA feed? Turkish has already started.

Asia Traffic In Transition. China-USA comprised 6 million annual leisure O&D passengers from the Middle Kingdon in 2017. Now it’s gone and not coming back. USA airline opportunities in China now gone. Future of trans-Pa will be business traffic mainly to SE Asia.

The eVTOL & Battery Propulsion Revolution: Answers, Please. To date, there has been no analytical support for this new air transportation concept. Year 2026 might bring some reality. Either way.

______

Monday Insight, December 8, 2025

Frontier/Spirit Combination:

Some Bullet-Point Observations

Square Peg. Round Hole. Makes No Difference, Anyway.

For the folks on the subscriber list for our weekly Touch & Go™ vision letter, the potential aspects of a Fronter/Spirit merger were outlined in some detail.

In as short and direct a manner as possible, let’s do a review.

Both Carriers Are Searching For New Strategies. Great. But neither one is compatible with the other, and both are exploratory.

Frontier is experimenting with micro-frequency impulse-dependent passengers generated by low fares, much of which is head-on with major network carrier hub-feed routes. In addition, markets of (hopefully) fare-impulsed demand are being added and deleted like bets on a craps table.

Behind all of this, analysts are pointing out that F9 profitability may be more dependent on aircraft deals than carrying passengers for the long term. Also, Frontier is still at the bargaining table with pilots. An agreement has been estimated by analysts such as Bill Swellbar to increase costs by over $100 million.

That’s one more factor usually missed in most analyses of these carriers: the low-cost part of the advantage is eroding.

Furthermore, it is questionable if adding a couple of ersatz first-class seats complies well with the intent to have system-wide ground-level, out-in -the weather boarding and deplaning. It’s also questionable if 29-30 inch pitch in economy, often equipped with a “tray table” only a couple of inches wide will develop strong business-category loyalty, especially on flights of a few hours or more.

Frontier is betting on mega capacity fleet iron. Of the nearly 200 airliners on order, approximately 125 are high-density 250-seat A321 variants. It’s not that this limits where they can fly so much as it dictates the markets where they must attempt to fly. These are routes with current heavy traffic demand – which in many markets is already served well by network airlines or are markets where low fares can generate huge chunks of new periodic passengers.

Trying new combination and approaches to customer service and route planning is a positive dynamic. But it will be challenging.

Spirit is retreating and circling the wagons (A320s?) around a market strategy apparently more based on developing brand identity in larger key leisure markets, with focus on FLL and the Caribbean.

It does understand, apparently, that routes that once had opportunities based solely on low fares – a.k.a. “the ULCC model” are becoming as dead as a dodo. Hence, a focused approach.

These two strategies – that of F9 and of NK – are as variant as a bus company from a commuter railroad. In any merger, it’s likely that the Frontier approach would be the one pursued. It’s one that does not need more airplanes or what exists of the Spirit route system. So, what’s the heavy benefit of going through the brain damage of a merger?

Weakness In The Impulse-Demand Sector. Much of the future of both of these airlines is dependent on having a huge gusher of discretionary dollars to be consistently generated by the national economy. This is not traffic generated by national air travel demand, but focused on very specific niches, some of which gravitate on economic factors that are potentially vulnerable.

One warning shot over the bow is Las Vegas. No point in going into all the drama, but as a low-cost vacation destination, it is declining fast. Visitors are down double-digit percentages this year due to the major changes in the LAS product. Dependance on generating new Las Vegas traffic is becoming slippery. One major revenue source heading downward.

Bottom Line: These are just a couple of core factors to consider when looking at these two entities. There are no – zero – market advantages to putting two carriers together, since they have differing strategic objectives and both are scratching for traffic, anyway.

The difference between these two carriers from Sun County, Avelo and Allegiant is that the latter three are not saddled with a lot of major past issues. They don’t have excess airplanes that desperately need a home. (The E-195 order from Avelo gives it two years to prepare carefully. Plus, they will be multi-role airliners. A 250-seat A321 is not.)

This is not rocket science. It is basic facts that traditional thinking is not capable of grasping.

The situation isn’t in doubt. Just wallowing in uncertainty.

Monday, November 24, 2025

Where The Smart Money Goes Sometimes Is Nowhere

I still am trying to get a feel for the scope we can expect in regard to the Advanced Air Mobility (AAM) concept.

I still am trying to get a feel for the scope we can expect in regard to the Advanced Air Mobility (AAM) concept.

There is no question that the concept of small aircraft silently whisking people and goods across metro areas is really exciting. The potential of new connectivity within regions is also innovation-provoking.

The only flies in this battery-powered ointment are little things. Like the cost and location of facilities to operate them. In a crowded city, will access to and from these AAM aerodromes represent more time saving and convenience. Then there are existing airports – what about the infrastructure to efficiently accommodate dozens of AAM aircraft and their passengers.

It goes on and starts to really muddy the fun.

One of the dynamics involved in these electric-aircraft programs is that there’s an ocean of smart money behind them. Billions of dollars from suitable and sophisticated investors and large corporations. That in itself should bring comfort to any open concerns about the future of some of the applications of small AAM birds.

Or, maybe not.

Anybody remember the initial concept for Eclipse Aircraft? It was to produce a really sharp 4-seat twin engine jet for something less than $800 grand. That was about a third of the cost of other available small bizjets.

Boyd Group International was engaged by an investment firm to do a high-level overview of Eclipse. To be clear, one ride in the airplane was enough to get anybody excited. Innovative proprietary avionics. A sharp luxury interior. Short field performance. As it stood, a breakthrough airplane.

Neat manufacturing breakthroughs like “stir-welding” (wow!). And comparing the price tag to other aircraft, it was a slam dunk. It initially sold well and had an orderbook roughly as long as an Iowa interstate highway.

Eclipse was enthusiastically backed by a whole phalanx of who’s who investors from the high reaches of industry. A business jet with these economics and costs was a slam dunk.

But it wasn’t, actually. The under $800K price started going up like a moon launch. Ultimately to over $2 million, which completely eliminated the single most critical value proposition of the plane.

Plus, any basic due diligence would have set enough red flags to furnish Moscow on May Day.

The initial engine – on which the low price was based – was found not to have enough thrust for the airplane to get out of its own way. That meant going to a larger, more powerful and more expensive P&W engine. The proprietary avionics were a problem. The production line was inefficient – it was taking days, instead of hours to mate wings with the fuselage.

The company did have success in bringing in incredibly experienced people to address this, but by that time the raw price of the plane was no longer a super bargain.

Today, the successor to the original is being produced, but not within the new market it was supposedly creating.

As you might guess, the bankruptcy filing of the initial Eclipse company didn’t do much to enhance the thrill for the original investors, and it delivered some headaches for folks who’d made deposits for airplanes not yet produced.

Aviation by its nature is founded on dreams. But not all dreams are founded on more than wishful fairy dust. In this case, it was visionary investors who got zapped.

Do a search. There are lots of these futurist projects now relegated to the closets of dead dreams, many of which were initially bankrolled by people and entities with a stellar track record of calling the right shots. This doesn’t mean that a lot of other such projects didn’t pan out, but this one is an example of how looking at an investor list is not a due diligence.

Not to be a curmudgeon, but AAM isn’t much different than Eclipse. A name list of rah-rah supporters does not relieve us of the responsibility to have at least some basic questions answered regarding a number of the assumptions supporting AAM.

This is not a criticism of the fine folks and corporations behind the numerous players in the eVTOL game. Investments in the future are positive.

However, the AAM is not just a visionary guy with an airplane concept. It is an entirely new system that will require massive investment and financial impact on USA airport and aviation infrastructure.

That means communities across the nation will have challenges at the local airport in preparing to accommodate and support AAM-related projects. Projects based on assumptions and good cheer instead of hard due diligence.

Maybe, ask how much per seat these eVTOL operations will require to make a profit? Other than minutes in the air, what would be the real travel time from Mid-Town Manhattan to the departure gate at JFK? Oops, what it the total environmental impact of huge fleets of battery-powered aircraft – from cobalt mine to cell production, to implementation of operation to disposition of used batteries?

Up to today, the prognosis for AAM is more like a pep rally than business analyses. The aviation media is more of a cheerleader at a soap convention. Mainline media like 60 Minutes have done gooey pieces extolling the program, without marring it with a single intelligent question. Financial analysts are almost giddy. Even the airport sector – where hundreds of millions of federal tax dollars are fixin’ to be spent on AAM facilities – is question-quiet.

Yes, I am aware that comments like these will lead to accusations of not being a team player.

And that is fully accurate, certainly when it comes to the consensus on AAM. Bluntly, I am not sure the team is fully aware of the rules.

Or where the goal posts are.

Standing by.

Monday, November 17, 2025

Former ULCCs On The Loose?

Over the past year, we’ve outlined how the traditional impulse-fare ultra-low-cost carrier (ULCC) sector was becoming less and less viable as a stand-alone sector.

Keep in mind that the ULCC model was pretty much a transportation system very distinct from network carriers. ULCCs focused on developing traffic generated by offering an alternative option for discretionary spending. Specifically, leisure travel, which in many cases would not exist in the absence of the low-cost leisure product offered by ULCCs.

It worked great. But the operational costs over time became a lot less “ultra” low. That, plus other shifts in consumer options, tended to take the profit rug out from under much of the ULCC model.

Extensive analyses of the financial underpinning of the ULCC model accomplished by Swelbar-Zhong have determined that it peaked roughly in 2023. Since then, the model has started to lose lift. We covered several aspects of this in the current Touch & Go™ vision letter.

A number of ULCC-model airlines have morphed to survive. The players have splintered off. Sun Country is quietly sticking to its MSP and cargo knitting. Allegiant is focused on its core Florida strengths. Avelo is planning to bring on new E195 E-2s into feeding leisure traffic into Florida from larger NE airports.

Then take a look at Spirit. Ten years ago, give or take, it was a profit machine. In the last 12 months, it has still been a profit generator. Mostly for bankruptcy lawyers. It has filed “Chapter” twice, has laid off hundreds of employees, dropped service at 16 cities (and counting) and shrugged a major orderbook for new airliners.

The airline continues to shrink down and fundamentally restructure its route system and market strategies. The route system cuts are not over. Nothing is sacred – the objective is highest and best use of resources and – not really noticed much – the goal is to showcase Spirit to the maximum consumer base possible. That indicates larger market populations are the objective for the planning future.

Spirit is obviously looking to refocus on South Florida, a market that’s only a leeeetle bit crowded. However, the key will be in building brand loyalty – i.e., customer service. To do it within a complex unbundled model is difficult.

Frontier has an interesting playbook. One that might be a new approach for the future.

Jamie Baker of JP Morgan observed that the airline has done well doing sales and leasebacks (SLBs) on its fleet, but it has done dismally in flying passengers. It commented, “the company’s aircraft trading business is profitable, while its airline business is not.” Actually, they projected that F9 could see as much as a whopping 34 cent per share loss in the core airline business in the 4Q.

The consensus seems to be that Frontier’s problem is industry over-capacity. When one looks at the airline’s strategy of jumping into routes already dominated by AA or DL (who are in most cases cross-supported by connecting feed), the traditional definition of “overcapacity” comes into play.

But maybe Frontier’s goal is really “opportunity capacity.“

Like, limited schedule frequencies that, using very low fares, can plumb some local O&D traffic that otherwise isn’t flying, or can be lured away from the dominant incumbent. Might have a play with couple of flights a week?

Maybe Frontier understands the market beyond accepted assumptions. The key will be seen in the next two quarters.

But one thing is certain. The traditional ULCC model is dead. But other models are in the works, maybe.

________

Monday, November 3, 2025

When Consumerism Goes Political

Airport Gate Access Legislation:

Start With Facts & Data. Not Inaccurate Blanket Assumptions

The issue of “equitable” access to airport facilities – mainly gates – has been on the front-burner for years. It is a valuable and important metric to consider.

But it must be based on hard facts, instead of assumptions and completely undefined terms. Just having an airline carrying “X” share of an airport’s traffic isn’t proof of anti-competitive activity or gate hogging. Indeed, it can represent a consumer benefit.

In our Touch & Go™ Vision Letter two weeks ago, we covered the recent wretch-worthy congressional hearings on the airline industry. The usual politicians wore out entire soap boxes with half-truths and righteous indignation about airlines.

In those hearings, a consumerist without a clue testified that American Airlines has been allowed to capture almost 90% of the traffic at Charlotte. Gasps and outrage!

Naturally, he left out the truth that over 70% of the airport’s passengers were due to American utilizing CLT as a connect point – a.k.a. hub – to feed passengers to other AA flights. These are people who have nothing to do with Charlotte except to cross the hall and board another airplane.

And, naturally, this clown left out that in establishing this connecting hub AA has delivered to Charlotte a couple dozen nonstop destinations that local O&D could never support.

This example is critical. The size and scope of an airline’s operation at a given airport is not a stand-alone metric that demands facilities be re-allocated. Yup, AA dominates CLT gates, but the truth is that to all but a few destinations, there isn’t snowball’s chance in Miami of another carrier being able to operate profitably based only on local O&D.

Point: the issue of gate usage is one of highest and best use for the consumer. Blind assumptions not based on hard facts and a keen understanding of air transportation economic realities are anti-consumer.

But that does not apply inside the Beltway. There’s now a bill in congress – titled The Airport Gate Competition Act. Boiling it down, it would require that 25% of airport gates be dedicated for common use and no more than 50% of gates be leased on an exclusive basis. This, the proponents claim, will foster more competition and deliver lower fares.

No analysis or factual review of the traffic base is necessary. No analysis of whether giving gates to other carriers will result in direct competition or cheaper tickets. No analysis of whether there actually are such airlines are waiting in the wings.

Nope. It’s all assumed. Good intentions are evident. But it’s a children’s crusade, not professional planning legislation, with a lot of well-meaning supporters who have not a shred of airline experience.

One of the sponsors of the Act is Senator Josh Hawley of Missouri. Typically, he’s a stand-up guy, but when it comes to the airline industry, he’s got a couple of loose screws. He’s torpedoed his credibility on the issue more than once. In particular, he has denounced airlines for refusing to quote fares until after the consumer first provides personal and other data to allow the carrier to adjust the ticket price accordingly.

Of course, it is completely dishonest and something that a quick visit to any airline’s website would debunk.

Yet, he’s sponsoring other legislation in this regard that is as misleading as this gate act. So, when it comes to airline issues, Hawley isn’t a credible source. He’s on a personal jihad, facts notwithstanding.

Certainly, to folks who are not knowledgeable in airline economics, what the Act suggests sounds fine. But it is founded on the unquestioned assumption that long-term leases are detrimental to competition per se, and they smother competition.

That assumption must be considered and factually reviewed on an airport-by-airport basis.

At Charlotte, imposing this legislation would be consumer averse. That might or might not be the case at other airports.

There is no question that if an incumbent is sitting on gate facilities and not fully utilizing them, and there are other carriers that can make better use of them, that certainly is an issue. But the Act assumes that is the case at all big airports.

More ominously, the belief also seems to intend that even if a carrier is making maximum beneficial use of gate capacity and delivering air access that other carriers might not be able to replace, it still should be forced to relinquish some of it to assure that more airlines can expand.

The Act postures that this will increase “competition” – with no consideration of what service would be operated compared to the existing incumbent.

Please, Act supporters, define exactly what “competition” is. If American is forced to give up gate capacity – even if it is fully and consumer-beneficially utilized – there’s nothing in this legislation that requires any analysis of what will replace it.

At airports where one of the big four – American, United, Delta, and to a lesser extent, Southwest have connecting operations, it is ignorant to simply assume that taking gates away will open new competitors to enter and lower ticket prices.

Let’s take what United recently announced at Chicago/O’Hare. New nonstops to at least seven smaller communities across the nation. This will open up new national and global access for Paducah, Marquette, Lynchburg and several others that will have material economic impact on entire regions.

As the Act clearly identifies, airport gates have value Therefore, before a carrier is forced to give up such capacity there must be some set of metrics to show that there will be benefit to the flying public. Identify it. Quantify it. Gates have value, remember.

Get this. If United is forced to relinquish gates, and in the process precluded from delivering national and global access to some communities via its ORD hub operation, under this Act the airline taking over has no responsibility to offer new service that is equally or more consumer beneficial.

In particular, it’s low fare and “value” airlines that are typically assumed to be the beneficiaries of this Act. But they are not after the same traffic sectors as network carriers. So, one or two might be able to operate fare-impulsed flights to Florida, or other such leisure destinations. That’s their business model. It is solid and valuable.

But it is amateur lunacy to believe that, being point-to-point carriers, that they would ever replace flights to St. George or Eugene that United might have to drop. Those communities – far from Chicago/O’Hare – will take the hit. All due to some politicians wanting gate “fairness.”

That’s one of the many flaws in this Act. It assumes that long-term gate leases deter competition. It assumes that just redistributing gate capacity will lower fares. It ignores the consumer benefits that a robust hubbing operation often delivers, notwithstanding the fact that such inherently needs a lot of gate capacity to deliver them.

This is not to state that gate-hogging may not exist at some airports. But it is incumbent on the backers of this Act to deliver hard data and facts to illuminate it. As of now, it is mostly based on assumptions that are not proven and promise new consumer benefits that may not be in the cards. As noted above, one of the writers of the Bill has already been shown to play fast and loose with the facts.

So, yes. Let’s make sure airport facilities are used to the maximum consumer benefit. Let’s get on it now with an honest evaluation of highest-and-best use, based on hard consumer metrics – on both ends of any markets that might get axed due to gate re-distribution.

Again, re-write this legislation to be consumer-beneficial instead enumerating lollipop intentions that are not connected to economic air transportation realities.

Facts and hard professional data first. Applying blanket across-the-nation assumptions is fatal to the credibility of the proposed legislation. Get off the righteous soapbox and show some gumption to re-write this Act.

Otherwise, dump it.

________

Monday, October 13, 2025

As Long As EAS Is Under Media Scrutiny –

With the federal shutdown, a number of inhabitants of the Fourth Estate have jumped out warning that funding for the Essential Air Service program might run out soon, cutting whole communities into dank economic isolation.

Take a look at a couple of the headlines in the last two days:

Yikes. Fake news is running amuck.

Okay, this is a perfect time to cut to the chase regarding EAS.

The Alaska EAS must be separated from Lower 48 EAS. In Alaska, air access is truly essential. In the Lower 48, it is a completely different story. Therefore, these are two very different transportation modalities. In Alaska, it’s survival. No flights, no mail. No flights, the local grocery store is empty. In the lower 48 at worst, it is a long drive to another airport strictly to carry a few passengers in and out. Get he difference?

Get the media educated. In the lower 48, the lightweights in some sections of media equate EAS to the airport being open. A wallow in fake news. The importance of rural and small community airports is not dependent on whether there are a couple of low-ridership flights a day. Plus, the media – from national networks to the local weekly paper – must be clearly educated about the realities of air transportation. In many cases, EAS is a waste. They need to be culled out to protect the political viability of the program.

Define “air service.” Today, the idiotic concept is that the local small community airport just needs to have “flights” – regardless of where they go. The assumption is that this is still the early 1970s when there was interline connectivity. Air service must be shifted to air access.

Take the decision away from the local community. Yes. They are not qualified. EAS eats up national tax dollars. Therefore, the concept that the local community should be a primary input is stupid. The DOT needs to define and analyze what the community should be able to support and do so with the objective of gaining the widest accessibility.

Define the metrics and the objectives. The DOT needs to take complete control of the process. With the paucity of available carriers interested in EAS, the DOT should be the decision-maker in regard to highest and best use of EAS dollars. In short, it is the DOT that should define the specific service that the local community can support, based on connective access to the air transportation system.

More to come.

______________

Monday, October 6, 2025

Clown Show.

Some Interesting Takes From

The Senate Airline Hearings

For our friends who are on the distribution list of our weekly Touch & Go™ vision letter, we covered why this type of event only sends air transportation back, not forward.

Truly more proof that hard facts and truth are not necessarily in vogue when it comes to dealing with the changes in USA air service evolution.

Calm, Factual Testimony Not Appreciated. A few of the people testifying were clear and factual. The attendees from Allegiant and A4A stayed the course. But some of the others were embarrassing.

The august Senators on the dais were mostly ill-informed and, to anybody with a modicum understanding of airline economics, almost insulting.

If these guys were around in the early 1900s, they’d probably be holding hearings on how to bring back riverboats and wagon trains.

A Couple of Low Points of Interest:

Gate Bag Fee Piracy. As usual, Senator Josh Hawley came out swinging about how crappy air service is today. This is not to imply that in some cases, he’s on the money. But handling it rationally and with precision is not his forte.

His target was Frontier. It started with the legitimate point that F9 pays a bounty to its (apparently) poorly trained contracted gate staff to find any oversize carry-on in the departure lounge.

To Hawley’s point (which his angry babbling completely left out) Frontier’s policy in such cases is to not only collect a bag fee, but punish the passenger with a demand for (reportedly) $79 dollars, or else boarding is denied. If the passenger can’t cough it up, they don’t go. Don’t insult the world by saying that’s the cost of checking gate bag.Even if it’s a family of four, no pay, no go.

No question, this is the nadir of customer service.

Unfortunately, Hawley never got to that discuss this specific revelation. He was too wrapped around himself, descending into how Frontier abuses its passengers, without any attempt to tightly focus on how.

In response, the CEO of Frontier defended the policy, simply saying the passengers involved had not paid the fee – missing the clarity that there is a clear size requirement, and therefore intercepting bags larger than the gate sizer was valid. The punishment fee was not mentioned. The bounty issue and what it really represents in regard to how Frontier views customer service was also not mentioned.

But then the Frontier CEO raised the ante and actually validated Hawley’s intended contention about “lousy service.” He implied openly that passengers who show up at a Frontier gate with a bag even slightly oversize were intentionally trying to defraud the airline, referencing such customers – his customers – as “shoplifters.”

Cool. A new standard in customer service. Accuse that fly-once-a-year grandma with a carry-on an inch too big as being a planned criminal. That apparently includes everybody, regardless, who might have a bag with a handle an inch over the sizer. That triggers the contract employees F9 has at the gate to see dollar signs. Track down these scofflaws. Get the bounty.

(We could note that both United and American have removed gate bag sizers. Instead, they advise their gate staff to use discretion and err on the side of the passenger when appropriate. In our digital, video-record-everything environment, this won’t go unnoticed when consumers do any research of which airline to select.)

Lots of Revelations Here. Actually, Hawley was accurate, but he was so childishly wound up that he couldn’t illuminate exactly what some F9 customers are experiencing. Plus, when an airline CEO contends that his own passengers who miss a rule are intentionally trying to cheat, that is a message.

The Consumerist Jihad – Facts Don’t Matter. Then we witness a guy named William McGee, a member of some organization formed to protect people from nasty corporations. He told the world that deregulation had failed, mainly because airlines have been allowed to drop service at small airports, supposedly trapping millions of consumers.

The concept of air access regionalization wasn’t considered. Like the level of service people in Pueblo had in 1978 v today. Back then, a couple of flights at Memorial Airport. Today, in exchange for an additional drive time of about 25 minutes, deregulation has allowed over 80 flights at nearby Colorado Springs. Far more access.

This guy was clueless in regard to customer convenience and time-management and contends that airports like PUB should have the same level of access as a much larger population center nearby.

He then slit his own intellectual wrists by denouncing major airline “dominance” at connecting hubsites. His blind hate of large airlines obscured the truth that such traffic is delivered by the dominant airline and isn’t the result of a capacity assault to keep other carriers out. It is substantially connect traffic that has no realationship with the local population.

The coup de grace to this guy’s credibility was when he angrily denounced American Airlines for dominating 88% of all traffic at Charlotte. He knows or should know that about 70% of those passengers are there because AA routes them there to connect. They are not O&D, and if McGee’s veneer contention to end this AA “dominance” would denude CLT of dozens of nonstop markets that are dependent on flow traffic and benefit the CLT consumer.

There’s more credibility at a second-rate used car lot.

A4A: Why Try Logic With An Unruly Mob? A4A was represented by Sharon Pinkerton, whose presentation was simple factual statements regarding fares, gate access and service availability. One could argue that she could have been more forceful with hard examples and data.

On the other hand, given the tenor of the Senators and some of the others at the witness table, it would have been a total waste of time. Sorta like trying to sell Estee Lauder stuff at an Amway sales convention.

Low Fares Are Okay. Sometimes. Frontier’s CEO had some interesting points. One was that major airlines have massive credit card and frequent flyer programs that churn in billions of dollars a year. His contention was that these revenues allow the carriers to subsidize fares, making them unfairly competitive with Frontier, which is too small to have such programs.

Funny, some airlines have systems that let them offer lower fares, eh? To F9, that’s anti-competitive, and obviously only in place to stop competition.

To the consumer, there might be a different conclusion.

Distant Consideration. There are some analysts who contend that Frontier may be similarly benefiting from the millions they are getting from fleet sale-and-leaseback deals. That can be argued to be program that subsidizes the ability to price the product.

Academia: Don’t Bother With Transportation Realities. Naturally, the La-la land contingent, a.k.a. academia was present. This professor from Great Boiling Springs University (or something like that) did start by stating the testimony was his and had no connection with his employer. Very considerate, in that his understanding of air traffic realities was at the pre-school level.

Lamenting the decline in scheduled service at many small airports (note: not access at communities, but flights at the local airport) he proposed that all these deprived airports should be put on a list, and airlines (not defined) should be forced to bid on serving them.

The concepts of consumer preferences, air service alternatives, levels of frequency, connectivity, and other factors do not apply. After all, the entire foundation is the ignorant conclusion that just having “flights” is having air service, plus the dishonest contention that having no service at the local airport is the equivalent of an economic desert island.

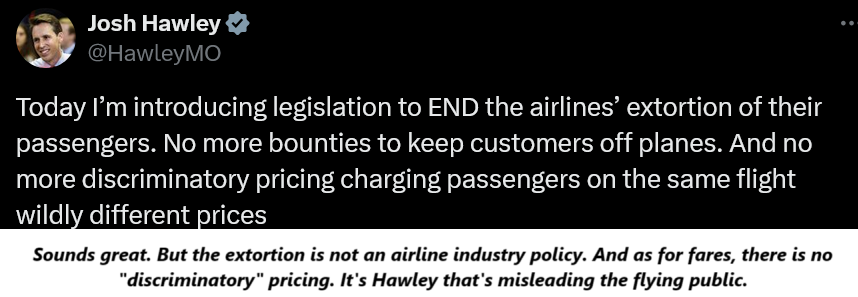

Nasty Dynamic Pricing. Like A Boogeyman Under The Bed. Finally, Senator Hawley finished the hearing. Still unable to focus even on real airline service shortfalls, he went into his trendy fantasy, accusing airlines of not quoting fares until the consumer provides personal data first.

As anybody out here in the provinces knows, when booking online, the fares are the first data shown. In all cases. From wherever the online web request is made. Hawley’s contention, in light of clear truth he’s ignoring, is a lie. There is no excuse for he, a US Senator, to not know better.

This was a fitting end to two hours of wasted time and misinformation and crackpot testimony.

The hard fact is that congress and the mainstream media are shamefully and intentionally taking air service and trying to pander to the public without having a clue.

And without concern for the consumer. Good intentions are demolished by political and technical ignorance.

The Senate should be ashamed of themselves.

______

Monday, September 22, 2025

Airport Security:

Signals Being Ignored

One of the biggest misunderstandings about aviation security is the nonsense that the goal is to simply stop bad actors from blowing things up.

That is just the most obvious part of AVSEC. But only a part.

The overall imperative is protection of aviation infrastructure, i.e., making sure that the facilities and systems on which safe operations depend are protected and secured from mayhem.

This responsibility includes more than screening people at check points. It’s also assuring the resiliency of the entire system.

This past week, there were two wake-up events that indicate the vulnerability that aviation faces.

One was a major security failure in the DFW Metroplex, where a phone line went down, tossing operations at DFW International and Dallas Love into chaos for several hours. Nobody was hurt. No violence. But it did shut the airports down pro tem. That means an area of vulnerability was not previously recognized.

As a matter of reality, there are lot of such areas, and most simply cannot easily be recognized. But that does not relieve us of responsibility to attempt to discover weak points on which aviation depends.

This is not to imply intentional human failure, but it does indicate the vulnerabilities the air transportation system faces. While it is natural to simply categorize this as a mechanical glitch, the hard truth is that the security of the system was breached.

Then take a look across the pond. Several large airports in the EU and UK were snarled by what was described as an intentional and selectively targeted cyber-attack. But not on the ATC system. Not on traditional airport security networks.

It is reported that the cyber target was the computer system that issues boarding passes and baggage tags. Since passengers could not be processed, the airports involved – Berlin, Brussels, London and maybe a couple others – basically stopped being airports and became short-term refugee centers.

But the domino effect of these shutdowns quickly zapped airline operation across and beyond Europe.

Everything else was not cyber-affected. But simply targeting the system that handles how passengers and luggage are processed at a couple of airports brought air transportation to its knees. Like, Copenhagen and Istanbul and Rome were reportedly not directly attacked, but the operational security of the entire air transportation system was flummoxed as hundreds of airliners got stuck on the ground at only a handful of airports.

These events should be a wake-up call for the folks running Homeland Security.

And for every airport in the USA, too.

Anticipation of security attacks goes beyond whether some clown can slip a Glock 40 through a screening point, or whether the airport perimeter is properly secured.

System operational vulnerability is also part of AVSEC.

The fear is that USA airport security planning is still based primarily on countering another 9/11 attack.

What just happened in Texas and in Europe tells us a new story.

Wonder if anybody is seriously paying attention.

Monday, September 15, 2025

Rural & Small Community Air Service:

Comfortable Snake Oil v Reality

Bad Planning Is Worse Than No Planning.

Just came across a website promising to be the tip of the spear in getting air service back to small airports. Not air access for communities but getting planes into airports.

Just came across a website promising to be the tip of the spear in getting air service back to small airports. Not air access for communities but getting planes into airports.

It’s called “Restore” – delivering a “plan” to get scheduled flights at the local airport, just like the 1980s.

The leper’s bell is going off. Y’all. The whole site is an electronic version of a South Pacific cargo cult. (Google it, if you must.)

Aside from the site being misleadingly festooned by 737s and even larger airliners, the message that it imparts is complete dreaming and entirely misleading. Right smack dab on the lap of the air service Santa Claus.

EAS & SCASD To The Rescue. Whoever authored this electronic candy assumed that all that’s needed is getting congress to slobber more money on the Essential Air Service Program. And they came across the Small Community Air Service Development Grant program as a solution, too.

Skyhook programs galore.

See, if these programs get funded with a lot more government gelt, the website assures us, airlines will just come a-runnin’ to initiate flights. No attempt at identifying anything more than “flights.” No discussion of whether there are such airlines out there. No thought of what alternative consumer air gateways are already accommodating local consumers.

Plus, it’s an inexcusable failure that no investigation was carried out to discover that the SCASD program has never been responsible for establishing service at any unserved small airport. It supported more service at Spokane. Got AirTran into Sarasota. Enough to convince United to add IAD access to MOB.

But small community airports? The program is a complete misfire. It is unfortunate that whoever put this site together didn’t bother with any research. It is appalling if some consultant is peddling this goo to these folks.

Not surprisingly, the airports and entities convinced to support this site back in 2023 have essentially seen zip in any material increase in major airline service. A couple have seen entry of Caravan service, maybe.

How ‘Bout Starting With Facts & Realities First. Rural and small communities need to take stock and understand that air access is the goal, and such service might be at a larger airport a long way off.

They need to be advised of the economic and operational realities of the airline business. They need to stop being misled into believing that there are lots of airlines out there and it’s a matter of just finding the right one. They need to define what “air service” is for a given community.

It’s positive that communities are aware of air service access issues. But when they get hornswoggled into believing raw economic nonsense such as this website, it is a scandal.

Point: a problem can’t be fixed when the facts are ignored. It’s been a couple of years since this site was established.

The results speak for themselves. Silence.

________________

Monday, September 7, 2025

Secondary Cockpit Barriers:

Secondary Cockpit Barriers:

One Tree In The AVSEC Forest

Coming up on 24 years since the 9/11 disaster.

Here is an important starting point: Think about this: after World War One, the French decided to build the Maginot Line. These were massive, reactive fortifications intended to address and prevent what happened and transpired after Germany invaded in 1914.

It failed because it was intended to address the past, instead of anticipating the future. Plus, the folks in Paris intentionally remained ignorant of changes in enemy strategies.

Tumble to this, as far as aviation security goes, the Transportation Security Administration is the USA version of the Maginot Line.

We are repeating history.

_____________________________

Southwest Airlines has put into service the first USA airliner with a secondary barrier to deter unauthorized access to the cockpit.

The impetus for this, obviously, is the 9/11 attack, now almost a quarter century in the rearview mirror.

This is a step in the right direction. But it illuminates how aviation security itself has been too often sent into the planning weeds by – I will say it – myopic, silo-focused programs that are like putting one strong link into a very weak chain.

The embarrassing performances on the part of the federal government subsequent to 9/11 were clear slaps in the face of the thousands who died due to known and accepted AVSEC failures.

The people at the top of the FAA – which was then responsible for aviation security – were political hacks who were never held to account, let alone removed from office. Most went on to cushy jobs at the newly formed TSA.

Actually, while the wreckage of the Twin Towers and the Pentagon was still smoking, George W. Bush was praising the FAA for its hard work. Hard work where incompetence and refusal to respond to known threats led to over 3000 lives lost.

Then we had the Charmin-thin and insulting press stunts, including staging national guard soldiers at the entrance to security check points, a placement that had nothing to do with what happened on that Tuesday morning. It was more of the incompetent “security” that was the cause of 9/11.

We could go on, but the empty suits who today proclaim that what has gone on in regard to AVSEC is a success, because there have been no such incidents in the last 24 years. Yup. Nor were there any in the 24 years before 9/11.

The implementation of secondary cockpit barriers is positive and necessary. But it addresses just one of the security failures that led to the hijackings. Great and good: access to the flight deck will be hardened.

But what about the rest of the aviation system? Most of the thrust of the TSA is in trying to prevent another 9/11, instead of implementing aggressive, anticipative security planning.

Like, understanding the intent of the criminals who did the deed. Hijacking airplanes and knocking down buildings was the M.O. they chose. Their objective was to destroy and kill.

Here We Are. Safe Behind The TSA’s Maginot Line. Do we really have anticipative airport security planning? What about event contingency planning and vulnerability identification?

Today, when a threat is discovered – after the fact – the program is to evacuate. Evacuate where? If an event takes place in Terminal A, what is the plan for the safety of the rest of the airport? Have any airports war-gamed and identified where the facility is vulnerable? The HVAC system? Location of trash cans? Screening of construction crews? And the list goes on.

New Threats: Are They Being Explored? Any thought given to the threat of drones? I said it before, but it is no big revelation. A creature from the Dark Side could certainly take easy aim at any number of USA airports. Think about the line of airliners waiting for takeoff at LGA at 8AM.

What we’re seeing in the Ukraine should be keeping airport and security planners up at night to work on identification of threat levels. How many airports have done any such exploration? Has the TSA considered any regulation or tracking of drone operations? These are no longer cute toys that can be delivered tomorrow via Amazon Prime.

How about emergency access and egress plans? There was a major bombing at Brussels a few years ago, and one of the main issues was getting emergency units to the airport. Anybody in USA AVSEC take notice?

Here’s the point illuminated by the installation of cockpit barriers: it is just one part of the security systems that need to be in place. But it is reactive to something that happened two decades ago.

Aviation security must be proactive and anticipative. It’s called planning, not reacting.

As we sit comfortably behind planning that’s geared to a single-event threat two decades ago, we are assured that our air transportation system is safe.

History is repeating itself. Think about it.

__________________

Monday, August 25, 2025

Las Vegas Going Upscale:

Las Vegas Going Upscale:

Watch For Falling Nonstops.

The web is rife with stories of how the traditional image of Las Vegas has evolved in just the last three years from $3.99 shrimp cockails and $8 all-you-can-eat buffets to $27 martinis and $80 prime rib.

Hotel rates now including daily “resort fees” of sometimes $50 or more. No more tacky show girls dressed up to look like designer ostriches. Fewer and fewer free lounge-lizards in the hotel bars. Blackjack with $20 to $25 minimum bets are more and more the norm. The image of the “rat pack” means nothing to today’s consumers, anyway.

Do a web search, and this is no mirage. Like the demolition of the hotel of the same name, this is for real. Video after video on YouTube validating sharp declines in crowds on the Strip, Downtown and in the casinos.

Point: ‘Vegas is no longer the take-a-cheap-weekend destination. The casinos and the attractions no longer are interested in the family of four coming for a fun few days. Or the college kids driving up from the LA Basin. No longer interested in price-driven clientele. No more minnows. “Whales” are the target. Heaven only knows where Circus-Circus is going to evolve. The kiddies and families it aims at aren’t going to be a growth segment.

That would mean that the folks arriving by air would decline. And it has started.

LAS is less and less an impulse market and more and more targeted to the Palm Springs and Monterey crowds. The average folks out in the provinces looking for an economic vacation are discovering that Las Vegas is not a welcoming destination. Florida or Arizona are.

And the gambling draw – always the lynchpin of ‘Vegas raison d’etre – well, it can be accessed today at any number of casinos across the USA, often at very upscale resorts that don’t gouge for parking and don’t have jive fees added to the room rate.

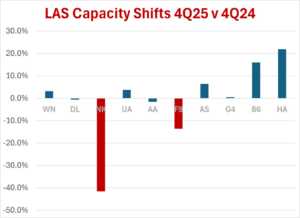

Using data from our friends at Airline Data, Inc, comparing 4Q 2024 to 4Q 2025 scheduled capacity, it would appear on the surface that things are adjusting. The LAS market as a whole shows almost a 7% total decline.

Using data from our friends at Airline Data, Inc, comparing 4Q 2024 to 4Q 2025 scheduled capacity, it would appear on the surface that things are adjusting. The LAS market as a whole shows almost a 7% total decline.

More cogently, virtually all of that decline comes from pull-backs at Spirit and Frontier. While there are strategic planning shifts at these carriers that are not due to the Vegas move into the upscale, it would appear that airline capacity – particularly that once supported by impulse travelers – is down big time.

Of note is the increase in capacity at Southwest. While the percentage is low, it’s still over 218,000 seats more that in 4Q 2024. To be sure, WN has been out of the ULCC or near-ULCC sector for at least a decade. However the trend at the other three network carriers is pretty much flat capacity.

Plan On Fewer Nonstop Destinations. Based on all the gloom-and-doom stories – which may be accurate, the reach of nonstop destinations will almost certainly decline in the near term.

There’s not a lot of high rollers in the Capital District eager to shell out $200 for dinner to support ALB-LAS nonstops, maybe. Same with probably a dozen or more such markets – the basic Las Vegas clientele are changing.

Point: Las Vegas is no longer the huge draw it has traditionally been. That means we will see further dilution of air service access. Not catastrophic, but the days of year-after-year growth are in the past.

__________

Monday, August 18, 2025

Airline Reporting: Caveat Reader

Fare Levels – It’s Not Just One Consumer Segment.

This morning, the Wall Street Journal carried a lengthy piece outlining how airfares are going up. It was replete with the perfunctory bar charts clearly showing the data month by month, as reported by the Labor Department.

Another Caveat Reader situation.

To start, they noted that travel demand had “wobbled” earlier this year. According to the article, this was due to consumers scaling back on travel due to their uncertainty regarding the impact of “Trump’s sweeping tariffs.”

That alone is lethal to the credibility of the WSJ article.

There is no hard data or reliable sources that show that the average consumer became reticent to travel because of tariffs. Most of the folks lined up at the boarding gates had no idea about what got “tariffed” in the first quarter and even what that means. Not a lot of “wobbling” going on.

It was a veneer trendy conclusion with no concrete factual support. Sloppy reporting – just feed it out as fact with no factual support. Indicative of the underpinning of the entire article.

The problem represented in the WSJ magnum opus was that the foundational assumption is that air fares are just one giant pile of ticket prices. The fact is that there are actually two general airline systems in the USA, and each has differing consumer pattern dynamics.

Each has capacity and route determinations very different from one another. Each with differing strategies affecting how they price their seats. To purport that it’s all one industry with uniform cost drivers is nonsense.

The headline itself was indicative of this journalistic failure. “Cheap Airline Seats Are Harder to Find.” Probably so, but what sectors of the demand for air transportation represented these cheap seats?

We are talking on one hand about traditional network carriers such as American, Delta, United and Southwest. (Newsflash to the WSJ: Southwest is indeed a network carrier. Check it out.) Then toss in the semi-network carriers such as Alaska and JetBlue.

On the other hand, we have the impulse (formerly called ULCC) sector, including Spirit, Frontier, Sun Country, Allegiant, Avelo and Breeze. It is the changes in this sector that will affect the supply of “cheap seats” – and much less so at the other sector.

Lumping the two together is indicative of poor understanding of the air transportation industry.

As we covered in this week’s Touch & Go™ vision letter, the dynamics and the shifting strategies of the impulse carrier sector are based on very different drivers compared to pricing decisions at United or American or Delta.

The point is this. The disappearance of “cheap airline seats” is different in scope and in consumer impact between impulse airline and major carrier systems.

The impulse carriers are focused much more on providing a limited destinational scope of capacity to a mostly leisure-based consumer base where the existence of the cheap seat is largely the demand driver. That’s also the case with what Frontier is chasing, which is capacity applied by limited schedule frequency in high-traffic major airline routes, with fares being the main marketing tool.

This is where the majority of the volatility exists in “cheap seats” – as clearly demonstrated by the 24% reduction in Spirit Airlines capacity. That reduction affects a whole different consumer genre that if it were at United or Delta. Those reduced seats mainly affect leisure traffic that is highly demand-based on the fare itself.

For another take, the newsworld is awash in articles chronicling how demand for ‘Vegas is down. That, by the way, is a bastion of cheap seats. One that is declining due to issues completely aside from the airline industry, but highly affecting impulse carriers.

Short of demonstratively outlining the differences in these two general airline structures, just tossing out overall fare data is only partial – at best – reporting.

It would be informative to have reporting that understands the current air transportation system.

Not to mention dropping babble that tariffs were strong drivers of people staying home.

Lightweight. And not informative, either.

Monday, August 11, 2025

Another Word on Southwest.

Controlling The Product Message

Is As Important As The Product Itself

The latest media coverage about Southwest is not comforting.

To start with, the lethal enemy of brand loyalty is anything that engenders “service anxiety” among passengers.

But it seems this is what’s happening at Southwest. The new “industry standard” product that Elliot is inflicting on the airline is taking a toll on a passenger processing system not geared for a lot of complexity.

It was one thing when Southwest announced the end of “bags fly free.” But that injected a whole new gate process that the carrier had never really had to deal with. They reportedly have implemented some kind of Ai program to “predict” when bins would be filled.

Apparently, it’s not working well.

Travel websites are carrying stories of passengers being required to check their carry-on at the gate, only to find when they board there’s plenty of overhead space available. That does not build brand loyalty.

In a situation where all the changes at Southwest are challenging the loyalty of long-time WN passengers, this kind of situation is not positive.

It is true that Southwest’s traditional model has revenue-atrophied. That doesn’t mean they were losing money they just weren’t making as much as maybe they could have been. The unfortunate part is that it left them vulnerable to invasive investors seeking not to improve the product but simply improve the revenue flow.

I know that sounds a little harsh, but the fact of the matter is when you look at the customer facing changes that have taken place at Southwest, virtually none of them have been PR-engineered into implying to the public that the product will be getting better.

Just go do a media check. Virtually every article about Southwest since the Elliot arrival has been about changes that are aimed at the customer paying more for less.

Build On Brand Loyalty – Protect It. Regardless of anything else, the approach should have been postured from the start to be part of a whole new Southwest that will be bringing the customer better service in the future. Not jive about passengers being able to sit together (like, maybe for an additional fee?), but hard reasons why Southwest is a better choice.

Think on-time. Think employees completely enthusiastic about their airline. Think consumer ratings. Think community involvement. These are absent or smothered by the media coverage going on.

The Traditional WN Market Impact Isn’t Possible, Anymore. The days when WN could enter a market and would magically bring low fares to town ended years ago. The days when city fathers believed that Southwest is the air service answer are ending fast.

The glow is gone, and that left the carrier vulnerable to the open cloak of entities seeking only to jack up share value.

J.D. Power Ratings: Don’t Get Comfortable. To its credit, Southwest just got top ratings from a J.D. Power survey. Great.

But remember that is based on perceptions that probably were ambient before the arrival of Elliott in the Board Room. The flood of negative media stories will – will – affect these perceptions.

And perceptions are affected by what people read and hear. Southwest has a valuable market identity position. They need to protect this asset.

It’s far more valuable than what Wall Street entities care about.

_________________

Monday, August 4, 2025

Aviation Security: Is It Time To Re-Think Awareness?

Aviation Security: Is It Time To Re-Think Awareness?

In light of the events in the Middle East, it has been suggested that there could be increased terrorist threats to our air transportation system.

An amazing insight into the obvious.

The question is whether aviation security is truly as well prepared as it needs to be. We were assured that it was before 9/11.

Warnings Were Obvious. So Was Political Incompetence. Most people are not aware that there were clear, obvious and announced warnings about what took place on 9/11. Despite this, airport security was politically assumed to be adequate, and such warnings were ignored at the highest levels.

Five months prior to 9/11, the airlines, FAA and the Massachusetts Port Authority were shown how vulnerable security screening checkpoints were at Boston’s Logan Airport.

The results of FAA inspections outlined by Red Team member Brian Sullivan revealed that security screening was shoddy and dangerously inadequate at Boston, and by reference, all USA airports. The message was not subtle: airports were wide open and vulnerable to terrorist attack.

The report made it clear: The risk was extreme, and what actually happened months later was clearly described as possible.

The team’s information was passed through channels. And completely ignored. The slop at screening points was emblematic of a security approach that had no accountability for professional performance.

But the Red Team’s superiors did nothing. Jane Garvey – the FAA Administrator at that time, and who was responsible for aviation security – did nothing.

Frustrated, Mr. Sullivan advised Senator John Kerry in a letter dated May 7, 2001. It was direct in warning the Senator that security at Logan was lax and warned him to imagine “a coordinated attack which took down several domestic flights on the same day.”

Remember, this was months before four airplanes were “taken down.”

As additional proof, his letter even cited a sting operation with a local TV station showing that in nine out of 10 tries, a crew got knives and other weapons through security checkpoints. Nine out of ten.

“With the concept of jihad, do you think it would be difficult for a determined terrorist to get on a plane and destroy himself and all other passengers?” the letter to Kerry clearly stated.

Mr. Sullivan did not mince words. “Think what the result would be of a coordinated attack which took down several domestic flights on the same day. With our current screening, this is more than possible. It is almost likely.”

And, indeed, it certainly was.

What makes it worse is that every single entity responsible for this failure has moved onward and upward after 9/11. With the exception, of course, of the Red Team and other related security people. They were disbanded and in some cased persecuted. (Read Fortress of Deceit by Bogdan Dzakovic.)

Garvey, who had the highest direct responsibility, has gone on to an illustrious career being a doorway mannequin for consulting firms wanting to show just how much clout they had/have in Washington.

Kerry went on to run for President. George W. Bush took no action whatsoever to determine responsibility at the FAA for AVSEC security failures. Indeed, in the days immediately following the 9/11 attack, he made clear he wanted to thank the FAA and the (inept) DOT Secretary Norman Mineta for their “fine work.” Plus, no one involved in the Federal Government was investigated or held responsible. Many went on to work at the new TSA.

What About Today? There Are Serious Misgivings. The TSA notwithstanding, airports, airlines and aviation entities are the ones responsible for AVSEC. They are on the front lines. The TSA isn’t – that’s a fact underscored by years of political management and a structure that is completely reactive. Deal with it.

So, the questions are direct to the front lines. Are there event anticipation, mitigation, and remediation plans in place – or at least considered – at our airports? How secure and monitored are known and potential access points? How vulnerable are emergency access and egress from individual facilities and terminals? How are airport staff and related companies trained in security awareness? Is the system ever war-gamed?

Lots of issues here. Waiting for the feds to tell us what to do, or tell us where the threats are, is irresponsible.

Deal with it: 9/11 was an example when professional terrorists took on and demolished USA airport security, which was run by politicians, not professionals. Airports and airlines must be security-professional, not obediant regulations-readers.

Airport Screening Isn’t Airport Security. It’s not the clown that left his Glock 40 in his carry-on that’s the threat. The TSA just loves to announce how many such weapons are discovered, and imply it was a terrorist, not some backwater yay-hoo moron not smart enough to pack his bag properly, that was apprehended.

The threats are from the terrorist A-Teams that want to destroy infrastructure and kill people. They are professionals, they plan well in advance, ascertaining where the system can be breached in the most effective manner possible. Aviation security must follow the same M.O. – think like a terrorist.

It is legitimate – no, imperative – that the airport and airline industries question what the TSA is doing. Question everything they put out. It’s not disrespect. It is learning from the tragedies of the past.

The history of the TSA in regard to airport security effectiveness isn’t particularly comforting. One reason is that there seems to be no transparent data available in regard to security effectiveness. Close as I can find, there is some information from ten years ago – where the TSA fell all over itself.

Subsequent to that, nothing.

Anybody have a question where that puts airport management? And where it puts airline security programs?

My suggestion: Go on to Amazon – get a copy of Bogdan’s book. Fortress of Deceit. It is truth that the media has conveniently ignored.

Ignorance is what allowed 9/11 to happen.

_____

Monday, July 28, 2025

AI Fare Programs:

AI Fare Programs:

When Monty Hall Becomes Director of Pricing

Delta’s intent to use artificial intelligence to determine individual passenger fares is going to open a whole lot of issues.

One is that it ex-post-facto validates a blatantly false accusation made against airlines, postured by a coupe of fact-challenged Senators.

Last year, Senator Hawley (R-MO) and Senator Hassan (D-NH) proposed legislation to stop airlines from continuing to demand personal consumer data before quoting a fare. This was subsequent to Senate hearings in December that would have made any marsupial proud. (Google it, if you must.)

Of course, the contention that airlines demand personal data before quoting a fare was a blatant lie. Not just misinformation, but outright false. It would take about fifteen seconds to demonstrate this by just going on any airline’s website. Personal information is requested well after the fare is shown. These senators aren’t too concerned about the truth.

But it was a convenient political soapbox. Airlines are convenient targets for political righteousness.

Back to the issue at hand. Once again, the truth is that airlines do not first get consumer data, and only then reveal the fare.

Warning. That may be changing to the point of shifting Hawley’s lie into the truth. Yikes.

Artificial Intelligence: Lots of Information. But Dangers of Abuse. Delta’s revelation that they are using AI to maximize revenues has just tossed a slow pitch to Congressional airline jihadists.

It is starting to look like Delta might be exploring how to set fares based on AI and other data that would reveal what the consumer is able to pay. Not completely clear, but it has successfully banged on the cages of several Congress dwellers.

The fact is that that fares are not set by personal individual passenger data. But the fear is that this may not be completely accurate for the future.