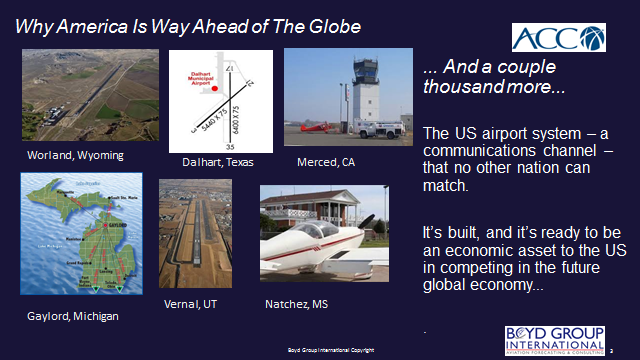

Worland, Wyoming…

Part of America’s Global Advantage

In this Update, we cover how the US has already built an airport system that makes it more competitive than any other country in the world in maximizing the future of the globa economy.

Yup. Worland. Please read on.

We’re constantly bombarded with lightweight media stories on how our airports have fallen behind the rest of the world.

The trendy comparisons are made using LaGuardia – which some nitwit politician a few years ago declared to be “Third World,” although the guy probably couldn’t begin to describe what that really meant.

But the comment got great, swooning and unquestioning press, though.

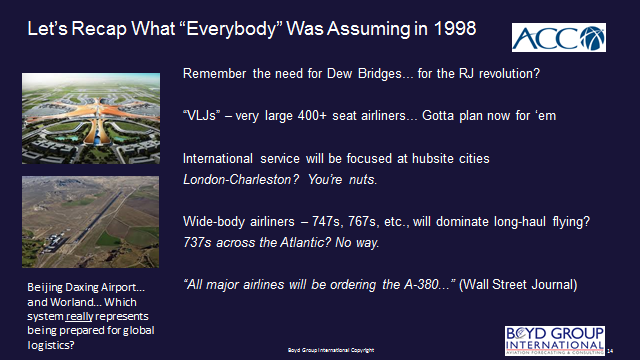

Then, as proof of our aviation myopia, we’re shown the sparking terminals at Beijing Capital, and at the new Daxing International Airport. Or, the new Istanbul airport. Or the wonders of the Incheon facility. Or the incredible shopping malls at airports like Hong Kong or even Heathrow.

America, we are told by the newly-formed airport-design Peanut Gallery, is falling way behind. This is often accessorized by really stupid comments inferring that any small airport without scheduled passenger flights is on the edge of total failure.

America, we are told by the newly-formed airport-design Peanut Gallery, is falling way behind. This is often accessorized by really stupid comments inferring that any small airport without scheduled passenger flights is on the edge of total failure.

But, like a lot of the media reporting today, it’s mostly just veneer nonsense. They don’t know what they are talking about.

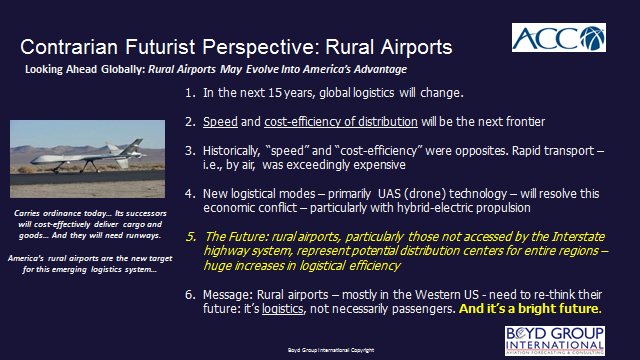

Fact: In the context of the future, and the new future technologies of trade and logistics, airports will be a critical competitive factor… America is way ahead of the rest of the globe, and far better postured for the emerging global economy. There is a lot more to our airport system than the parking convenience at ORD, or the snazzy people-mover at DFW.

Actually, these major airports are only one part of the US airport system. Our rural airport system is where the real advantages are – they will allow the US to be completely accessible to new logistical systems. No, scheduled passenger service isn’t in the cards, in most cases. New channels of communication are already making a lot of rural and intra-regional passenger air service non-competitive.

In the future, air logistics will be the difference in being competitive and being left back in the 20th century. The US airport system today – over 5,000 facilities – opens every corner of the country to potential access and benefit from this new global economy.

Airport Value Goes Way Beyond Passenger Service. What these parrots miss is that airports are not about the splendor of the architecture or the grand sweep of huge terminals, replete with glorious art work. Those are nice, maybe, but they are not the metrics on which to judge the value and efficiency of a nation’s airport system.

The only foundational metric is whether a nation has a viable airport system – and that goes beyond monuments to civic hubris and goes beyond the outdated and increasingly sham-infested concept of “air service development.”

Here’s some insight that goes beyond the day after tomorrow, which is the typical horizon of a lot of the current discussion on America’s airports…

The future of global competitiveness will be speed of logistics. Speed of logistics will be shifting to new modes of air transportation that will open whole areas to new development – but that requires an airport system that’s built, efficient, and ready.

Across the globe, only the United States is ready for this.

A Couple of Points… In November, we were honored to deliver the keynote address to the 40th annual meeting of the Airports Consultants Council. Here are some of the key points that Boyd Group International would illuminate in regard to the future.

We mention Worland… it’s just one part of the gigantic US airport system. The USA has over 5,000 airports. China has 300. The USA’s airport system will open all parts of the nation to the new systems of logistics. As we’ll note below, the cost differential between air logistics and ground will materially diminish in the next decade, illuminating potential for communities across the country to be part of the world commerce system.

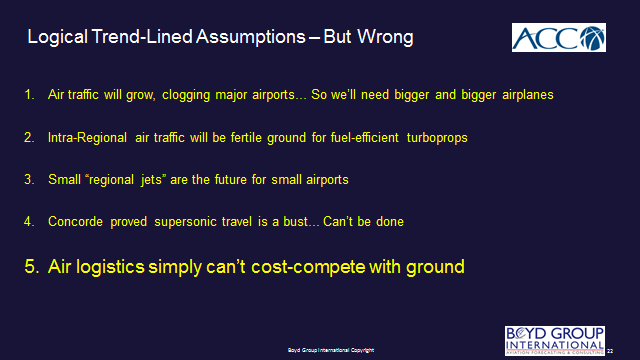

Most of the planning assumptions that were in play 20 years ago now look a bit ridiculous. That’s normal – the future cannot be completely forecasted. But then and now, every assumption needs to be put up against emerging global transportation and trade shifts.

Every one of these made sense in the context of twenty years ago. But today, airline fleets are size-compressing – at both ends of the unit-size spectrum. Supersonic air transportation is back in the play. But the main issue to consider is #5 – speed is the #1 competitive factor, and it’s shifts in propulsion technology that will revolutionize air logistics.

There is no such thing, anymore, as a US automobile. The parts and components come from suppliers based and/or headquartered around the world. This means that transportation and production efficiency will be determinants of where production and distribution facilities will be located. It’s already starting to happen. With advances in UAS technology, locations like Worland and New Braunfels, and Gaylord are all in the hunt.

Yes, this is contrarian… but in the context of today, most of the future is contrarian.

The full presentation made to the Airports Consultants Council can be requested by clicking here.

But the main concept to consider is that in the global future, air logistics will be a critical component of competition. And, regardless of what happens rebuilding LGA or JFK or MCI, the USA is ready.

We’ve just made available our Summary report of the trends emerging as we come to the close of 2018.

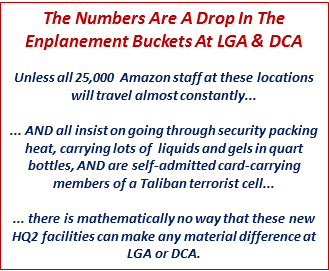

We’ve just made available our Summary report of the trends emerging as we come to the close of 2018. Yessir, there’s going to be a tsunami of new airline passenger traffic generated by the decision by Amazon to locate facilities in Queens and in Northern Virginia, promising to bring an additional 25,000 jobs to each region.

Yessir, there’s going to be a tsunami of new airline passenger traffic generated by the decision by Amazon to locate facilities in Queens and in Northern Virginia, promising to bring an additional 25,000 jobs to each region. Some will be from Queens, some from other Buroughs, and some from Long Island and elsewhere in the region. But most won’t be arriving in moving vans.

Some will be from Queens, some from other Buroughs, and some from Long Island and elsewhere in the region. But most won’t be arriving in moving vans. anything produced by Boeing or Airbus or Embraer.

anything produced by Boeing or Airbus or Embraer. Let’s not forget the planned Sino-Russian wide-body C929 that’s also a glimmer on the long term horizon. Or, maybe we should.

Let’s not forget the planned Sino-Russian wide-body C929 that’s also a glimmer on the long term horizon. Or, maybe we should.