sd’;flasd;fsd’f;sdf

Author Archive: Mike Boyd

Monday Update January 7, 2019

Seven Trends That Will Affect Air Traffic In 2019

Looking at the New Year, BGI has identified Seven Key Trends that will have material effect on US air transportation…

One: The Threat To The Drone Revolution

Two: Airlines Now Much Less Affected By Outside “Studies”

Three: Northeast Airports In Line For Trans-Atlantic Service

Four: US Carriers To Reduce China Capacity

Five: The Iceland Hopscotch System To Europe Is Ending

Six: Cuba: Less Service… The Expectations Were Bogus

Seven: ULCCs To Be 15% of Capacity… But Where?

Let’s take a look:

The Drone Revolution: Time Is Running Out

The potential is incredible – particularly for the new economic role of rural airports.

But what’s also incredible is the fact that the FAA simply views it as just a bunch of small flying machines that are mostly interruptions of their day.

There are now thousands of un-tracked drones in use across the country, and the recent examples in the UK and China, where they were used to threaten operations, are just warnings.

It’s not just a matter of detecting these things. It is imperative that systems be found – now – to be able to identify the operator.

Unless the FAA gets off its keester and starts to take some proactive leadership in developing controls and monitoring of these devices, the chances of a nasty drone-airplane accident are going up by the day.

The FAA has no grasp of the importance of this new technology, and zero understanding of how to deal with the challenges it represents.

One accident… one near-miss… one terrorist use of a drone, and the clowns in Congress can be depended upon to use it to the utmost political advantage.

Point: the various sectors of the UAS industry need to continue to aggressively take these issues into their own hands… waiting for the FAA to do it is like leaving the light on for Jimmy Hoffa.

_____________________

Airline Planning – Increasingly Unilaterally-Generated.

In 2018, there was a marked change in airline route and market tactics.

It’s now clear that major carrier systems each have their own clear, set-in-stone route strategy. They’re not looking for outside advice – their plans are in the works already.

The imperative for airports in 2019 will shift from the outdated goal of “making the case” for a random new route, to accurately predicting, identifying and matching carriers’ evolving growth strategies.

That 60-page “true market study” may impress the mayor, but it’s no longer a Delphi-like revelation to airline staff. They have their own strategies… airports and communities must now identify and adjust to airline direction, not the other way around.

Market-Matching The Fleets. The key is to understand and anticipate how fleet shifts and aircraft utilization will drive market decisions.

A couple of examples. Take a look at United: they are adding A-319s coming off lease from carriers across the globe, but on the mainline side, they have very few portions of their fleet that are in line to be retired. Message: at some point, there will eventually be the specter of reduced dependence on outsourcing flying to other operators.

Delta is now pulling down the fleet of 717s they acquired from Southwest, and adding in A-220s, while also reducing both MD-90s and MD-88s. This does indicate a different set of route and market strategies – because the new fleets represent new market missions and market applications.

As for 50-seat jets, they gained a reprieve with lower fuel costs. But that’s still temporary… they will be phased out at some point in the future, and it will take place with not a lot of early warning.

In 2019, major fleet mix changes will identify airline strategies – and route planning – for the future.

Get Out of The “Study” Trap. In 2018, Boyd Group International was successful in assisting a range of airport clients in building new air service access, using this approach. If your community is interested in getting right to the chase in regard to crafting a futurist air access plan, give us a call, or click here for more information.

We know airline strategies – and, as demonstrated at our International Aviation Forecast Summits – airlines know us.

___________________

Expanding In 2019: Trans-Atlantic Flying

Boyd Group International was the first to outline the potential that large non-hubsite US airports represented to EU and UK carriers.

That’s now taking place.

The next phase – which BGI forecasted at the 23rd International Aviation Forecast Summit last August – is trans-Atlantic service from secondary US points along the US East Coast. The economic factors will be generated based on regional access to strong internationally-related business and industry.

Charleston-London is just the first… and the metrics airlines use to determine these markets differ from traditional ones.

Road-Hubbing Airports In The Cross-Hairs. Here’s a hint on what to expect: draw a radius across the Atlantic from London based on the range of the new long-range A321Neo.

Take a look at the US airports that are covered. Then take a look at the interstate highway access they may have, and draw a 90-minute drive time from there, and compute the industrial base. That’s the raw starting point for developing and honing the true new trans-Atlantic catchment areas.

Using traditional metrics, there’s no way Charleston could support London service. But those metrics and that approach are now obsolete.

Point: there are about ten airports in the Northeast that may want to make sure their FIS is ready, and they have the political juice to get them staffed.

Get Your International Program Going. Boyd Group International’s Airports:USA® and Aviation DataMiner™ systems have the futurist analytical capability of determining approaches airports and regions can take to attract this new international dynamic.

Give us a call or e-mail, and we can discuss developing a community outreach and airline industry strategy for your region.

______________________

China: US Carriers May Need To Temporarily Retrench

Our forecast for US airlines: be ready to cut China capacity in 2019.

The local US originations are likely to fall precipitously in the second quarter of the year.

No, it’s not due to trade disputes.

It’s going to be driven by new policies by the Xi administration in Beijing intended to crack down on dissent, and which have resulted in the US State Department issuing a warning regarding travel to China.

“U.S. citizens may be detained without access to U.S. consular services or information about their alleged crime. U.S. citizens may be subjected to prolonged interrogations and extended detention for reasons related to “state security.” Security personnel may detain and/or deport U.S. citizens for sending private electronic messages critical of the Chinese government.”

This will have a chilling effect on visitation from the US, and that will hit US airlines harder than Chinese carriers. The chances of a US visitor to the Great Wall to get involved in any of this are pretty slim, but the implications are not such as to get folks to get enthusiastic.

BGI has been at the forefront of analyses of the booming Chinese air transportation system, and the huge potential for traffic from China to the US. We are the leader on China consulting for US airports and communities.

Chinese Visitors Will Keep Coming… But On Chinese Airlines. We previously were predicting over 25 million folks from China to visit the USA over the next five years. For the time being, that forecast stays in place. The demand from China, given implementation of nonstop flights from key cities to large US commercial centers, is still astronomical.

Just one example is Fuzhou-JFK. (Yes, Fuzhou – google it if you must.) Before Xiamen Airlines implemented nonstops, the total O&D between these cities was estimated at less than 3,500. In the first year of nonstops, Xiamen carried over 70,000 passengers – all O&D.

So, the curious projection is that China-originated US traffic will not be materially affected. But US airlines likely will see some downturn in the coming months.

_________________________

End of The “Iceland Option”

In 2019, we will likely see the end of the “Iceland-Option” – really low fares to Europe – in exchange for a stop in KEF.

Like with domestic ULCCs, the lure of super low fares as an alternative spending option for a trip to Europe looks great. But that concept also encompasses the need for the destinations to be well-accepted and desired.

Phoenix, Orlando, Punta Gorda… no problem. But for consumers in the US, going to places like Cork or Oslo at cheap fares, with a stop at an airport many can’t spell, let alone know of, hasn’t translated in the same way as an impulse trip to Epcot.

By the end of 2019 – most of the Iceland-US service to non-hubsite airports will be gone.

___________________-

Cuba: Move Along, Folks. Nothing Here.

Or, Not Much To Visit, Yet, For That Matter

In 2019, there will be more constriction of US-Cuba air service into the SE Florida – Havana corridor.

As has been forecasted in studies by BGI, Cuba “demand” is several galaxies away from the euphoric nonsense put out by the travel industry immediately after the “opening” of the market by Obama in 2014.

FedEx recently gave up on attempting cargo services, noting that they had difficulty in finding local partners to work with… not to mention the challenge of finding any cargo business, either.

Attempting air freight operations to Cuba is akin to shipping air conditioners to the burgeoning condo market in Antarctica.

Southwest recently dropped plans to add more Cuba flying out of Tampa, and American is tossing in the towel on CLT-HAV flights. Alaska, Frontier and Spirit have left the market.

Contrary to implications in some parts of the media, this has nothing to do with any revisions made in Cuba travel policy by the Trump administration.

The market will remain a dog until cleptocracy running the place opts for a new line of work someplace else. There is no business base in Cuba, and give-or-take a couple of high-profile hotel deals, the hospitality industry is somewhere still in the 16th century.

2019: The focus will be on SE Florida to Havana, and most of that will be VFR and adventure travel.

_______________________

ULCC Capacity: How Far Can Fare Stimulation Go?

Projection: ULCC capacity will grow to as much as 15% of all seats produced in the US by the end of 2020.

Other than a complete economic downturn, this may be conservative. However, this will not alter the need for a shift in economic planning from often-futile attempts at getting network service at small local airports, instead of wider, regional approaches.

In 2019, it will take a Ouija Board, a crystal ball, a gypsy séance and several e-mails from On High to predict where ULCC service will spike traffic, and which routes will see those spikes deflate as these carriers rapidly re-deploy assets.

But it won’t take much to understand that there will be enormous amounts of net-new air traffic generated by this genre… which now includes Sun Country, joining Spirit, Frontier and Allegiant.

A Short-Term & Long Term Forecast Tool Now Available. The challenge for airport planners is to attempt to project where and how these carriers will increase enplanements.

The Boyd Group International Airports:USA® program aggregates a wide range of near-term metrics at each US airport, including factors such as capacity shifts, load factor trends, fare level sensitivity, and other data, to produce our exclusive Short Term Enplanement Trend Forecasts, looking 12 – 14 months into the future.

Updated monthly, the program delivers a reasonable projection of traffic volatility, and then is the basis of the Airports:USA® ten year forecasts.

If you are not an Aviation DataMiner Subscriber, click here for more information on our short term and long term enplanement forecasts.

______________________

More B-717s Retired

Last week, Delta parked another three of the -717s they acquired from Southwest. In addition, they are slowly pulling MD-90s out of their fleet.

Monday Update – December 31, 2018

The Year Ahead – Fasten Your Seat Belts…

Next week, we’ll be posting Boyd Group International’s 2019 Aviation Projections

Some issues we’ll be covering…

The FAA’s Threat To The Drone Revolution: The potential is incredible. But what’s also incredible is the fact that the FAA simply views it as just a bunch of small flying machines that are mostly interruptions of their day.

Their lack of aggressiveness and vision is putting not only this industry, but aviation safety, at risk.

Aggressive Internally-Generated Airline Strategies. In 2018, there was a marked change. It’s now clear that major carrier systems each have their own clear, set-in-stone route strategy. They’re not looking for outside advice – their plans are in the works already.

The imperative for airports in 2019 will shift from the outdated goal of “making the case” for a random new route, to accurately predicting, identifying and matching carriers’ evolving growth strategies.

That 60-page “true market study” may impress the mayor, but it’s no longer a Delphi-like revelation to airline staff. Airports and communities must now adjust to airline strategies, not the other way around.

Two words: emerging airline fleet trends. We’ll look at this next week.

ULCC Wild Card: The ULCC product is largely based on impulse spending. When the economy is strong, there are lots of discretionary dollars in the market. When it goes up or down, ULCC traffic will be one of the first harbingers of the change.

Point: The US is facing a continuing strong economy and consumer confidence. Draw conclusions accordingly.

End of The “Iceland Option.”. Oops. The ULCC concept is based on more than just super-low fares. It also demands simplicity and familiarity with the destination. We’ll look at the collapse of the “Iceland-Option” – really low fares to Europe – in exchange for a stop in KEF.

But for consumers in the US, going to places like Cork or Oslo at cheap fares, with a stop at an airport many can’t spell, let alone have ever heard of, hasn’t translated in the same way as an impulse trip to Orlando.

Emerging Uncertainty Regarding China-US Travel. BGI has been at the forefront of analyses of the booming Chinese air transportation system. We previously were predicting over 25 million folks from China to visit the USA over the next five years.

We are the leader in advising airports and communities in crafting China-outreach.

But we are now suggesting caution… there are very real and very disturbing developments that may choke growth of China-US air passenger traffic – in both directions. Not to mention further Chinese business investment in the US.

And it has nothing at all to do with any US-China trade issues.

Message to US airports & communities: don’t jump into too many “trade missions” to China in 2019, without first getting a hard and honest view of what’s unfolding inside the place.

We will outline the emerging changes in this market. Not encouraging.

The Next Phase of Traditional EU Carrier Invasion. Year 2019 will see the new trans-Atlantic nonstops – particularly from secondary points on the East Coast. The dynamic of “road hubbing” will figure large on the whiteboards in planning departments at EU and UK carriers. Whole new market-decision criteria.

We discussed this at the International Aviation Forecast Summit last August – and it’s going to accelerate in 2019.

Think: Route capabilities of the A-321Neo.

More… Year 2019 will be one of change – mostly positive.

We’ll discuss these issues – and others for the New Year – next week.

Monday Update – December 24, 2018

UAS Technology Is Huge – But Until Drones Can Be Monitored – Ground Them. Now.

Drone Technology: A New Communications Channel That Will Transform Logistics.

But For Now, Ground Them.

Flak… for all those playing the home game, it’s short for Fliegerabwehrkanone… a weapon that ultimately splattered the sky with small metal pieces– maybe 3-6 inches long – pieces meant to hit and down aircraft.

Drones – UAVs – small flying machines weighing as little as 5 or ten kilos. They can and have gotten in the way of airplanes. Kinda like flak, ‘cept they’ve not knocked any airplanes out of the sky.

Yet.

Stealth Operators & Almost Stealth Machines. While there are significant differences between a lightweight drone and the ordinance shot off by a German 88, the one thing in common is that they both represent objects that are threats to air navigation. And, unlike the flak version, there is no way of telling who’s tossing them into the sky, or from where.

The recent shutdown of London Gatwick Airport due to the presence of unauthorized drone activity is a final message – one that the FAA has consistently been dodging.

Let’s put this in context… Reports of little devices buzzing over the airfield have just shut down London’s #2 airport for a couple days because nobody could trace where they were coming from or where they were going. More critically, the operators were almost 100% assured of having complete safety from being traced.

Not a bad M.O. for a lunatic or a terrorist.

An Imperative Security & Safety Issue. Despite some panting media stories, this is no grand revelation. Two airports in China were repeatedly affected last year due to untraceable drone activity. There are already reports of aircraft colliding with these devices. It’s been going on for years. Regardless of reports from London that maybe the sightings were just the result of some people’s imagination, the fact is that this type of event has happened elsewhere.

More and more of these privately-operated machines are being bought and used. Sure, the FAA in its wisdom has regulations on their use. But that is entirely different from controlling and monitoring how and who is operating these contraptions.

Tumble to it: It’s only a matter of time before there is a fatal event – accident or intentional.

The message is that drones can easily be used improperly and, worse, as weapons. At London Gatwick, the incident was essentially using drones as instruments of terror. In this case, nobody was killed, but it successfully made an entire airport inoperative. Point: that is the goal of terrorism, which is to shut down our systems.

A Growing Security Time Bomb. Conclusion: At least for the time being, privately-operated drones must now be banned – taken out of the skies – until and unless there are mechanisms in place to be able to easily detect them, and – far, far more importantly – ways to immediately and consistently trace where they are operated from.

A Future Transportation System In Jeopardy. It also is now incumbent on the leaders in the UAS industry to make detection systems – both of the unit and its operator – their #1 priority. That’s because the entire drone concept is one that in the future can have enormously positive effects on commerce and trade.

But just like horseless carriages needed to have new sets of legal controls, so do drones. Regardless of the size of the UAV industry, and regardless of how many folks have bought these devices, they need to be prohibited until such mechanisms are fully in place.

FAA & Homeland Security – Professional Cadavers. ‘Course, the FAA is still off in la-la land… here’s one of their shallow-end comments…

“Generally, drone operators should avoid flying near airports because of other air traffic. It is very difficult for other aircraft to see and avoid a drone while flying, and drone operators are responsible for any safety hazard their drone creates in an airport environment.”

“Generally…?” Is there anybody awake and sober in the front management offices at the FAA? In the context of how drones can be used to create mayhem, the FAA’s out to lunch. Just like they were before 9/11, when they were responsible for aviation security.

Back then, they couldn’t hear thunder, and they ignored repeated reports regarding sloppy airport security. Today, they and their demon spawn from the outcome of 9/11, Homeland Security, are just as numb to reality.

A Promising New Communication Channel – But Not Yet Safely-Ready. This isn’t a suggestion that will be met with much enthusiasm from the folks in the drone industry. Or some businesses that have spent a lot of money preparing new applications for these machines. That’s understandable, in that they fully recognize that this is a technology that represents an incredible new communications channel.

As Boyd Group International has pointed out, combine this with the 5,000 airports in the USA, and this could be a whole new logistics system that eventually will be competitive with ground transport. At the 20th International Aviation Forecast Summit in 2016 at Las Vegas, we had an extensive workshop on the entire UAS future… and it is incredible what it represents.

As a harbinger of this, there’s already a small Chinese airline that is reportedly converting old AN-2 type biplanes into drones to deliver goods and cargo to remote communities that barely have a gravel strip. Imagine what new-technology drones, particularly with hybrid powerplants, could represent in the US.

But all that future is now at risk until the security issues with drone technology can be addressed.

In the meantime, the responsible action is to prohibit all commercial and private use of drones, before there is a body count.

One incident, and you can make book that the inhabitants of the Marble Playpen in Washington – also known as Congress – will stampede in all directions like a herd of self-righteous water buffalo, to completely ban any drone usage in the private sector. They could kill off the future that this technology represents.

The new imperative is to find solutions ASAP.

In the meantime, take these devices out of private use.

More Air Service Access Success For BGI Clients

We are excited to note that Traverse City will be gaining first-ever nonstops to Washington this summer, with United adding week-end frequencies.

This follows United planning nonstops to Denver this summer.

At Manchester, American Airlines will be adding daily flights to its global hub at O’Hare.

If your airport is looking for results, consider using BGI…

The difference in BGI air access programs is that we go directly to the target carriers with hard data, and skip the traditional, unfocused and expensive “true market studies” that airlines smile at but at the end of the day pay no real attention to.

Give us a call, or e-mail Dan Cohn by clicking here.

Biometric Airport Processing

It’s here. Using facial recognition to process through airports. Delta is implementing it at one terminal at ATL. American and JetBlue are pursuing it. Hertz, too.

Starting a new age of Big Brother? The start of what China is (unfortunately) pursuing – a complete on-going social scorecard, monitored by the government, based on a national ID card?

No… it’s really just replacing paper and using data that’s already recorded. BGI’s Mike Boyd recently spoke with CNBC on the subject. Click here & take a look.

Monday Update – December 17, 2018

More On The 40 Years of Airline Deregulation – We Take An Iconoclastic Review of 35 Airline Start-Ups That Went Down The Tube & Into Aviation History.

Better Air Access, But Lots of Start-Up Wreckage

A Review of Selective Airline Start-Ups Since Deregulation

It’s been four decades since December 15, 1978.

From that date forward, the airline industry was open to new competition. The assumption was that new airlines would spring up all over the nation, to go head-to-head with established legacy carriers, and bring lots of new consumer options.

Spring up they did. But not many went much further. Most went down like a baby grand out the 10th floor window – the victims not of competition from legacy carriers, but from self-inflicted folly, bad planning, and inept management. Arguably, no industry has likely seen so many start-up failures as did the US airline industry subsequent to the Deregulation Act… roughly from 1979 and 2000.

Airlines 1979-2000: Economic Darwinism At Its Height

Actually, those who lament that there are only about nine major airlines left miss the fact that, because of deregulation, these now offer better air service than that which was possible when the feds had their fingers in how and where airlines should fly. Less airline brands, yes. But competition is there.

One thing unforeseen in 1978: New entrant carriers actually did not become a major part of the evolving Deregulation scene. Actually, most of them went down the financial ceramic fixture, as we’ll discuss below.

Changes In Air Service – A Lot Due To New Communication Channels, Not Deregulation. Yes, there may be less local air service at some small communities – but, contrary to civic hubris and pandering consultant studies, in many of these cases, it’s the consumer that has made the decision, and for them there are now better and more time-efficient air service options elsewhere – even in some cases with a 90 minute drive.

Not only that, but with new communication channels, the need and the value of doing a day trip between places like Albany and Buffalo have become far less cost-effective than 40 years ago. Frequent consumer service in markets like this isn’t coming back

The fact is that the economics of air transportation and the changes in communication channels have now made consumer-acceptable air service at many local small-community airports financially impossible.

There Are Whole New Consumer Options. As for engendering more new future airlines – it’s the economics of the marketplace that will decide, not political intervention. We have seen JetBlue and Virgin America come along in the traditional space – in the latter case so successfully that it was eagerly sought as a merger partner.

In the new impulse-buy segment, where price is being used to stimulate air traffic that otherwise would be staying at home, we have mostly leisure-focused service from Spirit, Allegiant, JetBlue, Frontier and Sun Country that has generated millions of new air travelers. The freedom to enter and exit markets without government influence has transformed air trips into a discretionary-spend option not possible in a regulated environment.

It is unfortunate that many politicians are myopically claiming that deregulation has harmed the nation. That is nonsense. After 40 years, it has brought market reality to the business, and consumers are the beneficiaries.

Consumers Often Have Better Options Other Than The Local Airport. Yes, some local airports at places like Topeka, or Youngstown or Pittsfield no longer have scheduled flights, and it’s a near-certainty that a return of such service is but a political pipedream. But their consumers today have robust air access to and from the rest of the globe at other airports that are not much time-farther away than are consumers in Suffolk County from LaGuardia.

Start-Up Failures – Non-Events. Keep in mind that all of these failed upstart carriers were on the margins of the air transportation system, and were essentially side-shows as competent airlines continued to grow and expand and bring wider global access to the US.

But the good news is that most of the lunacy in regard to airline start-ups has run its course. The cost hurdles to get into the business are enormous, and there’s no more room or financial tolerance of amateur act airlines.

But it was interesting – like the airline that turned itself over to what they thought was a big money man, who turned out to be a 19 year-old kid. Or the airline that zapped one community and state for almost $47 million, with the promise of creating jobs. Or the once-global iconic airline which is now essentially a rural freight railroad. Lots of fun and games.

But give or take a Skybus – which included crackpot features like hawking consumer products in the cabin – or a recent regurgitation of the name PeoplExpress that redefined the term “inept,” (neither covered here) it’s unlikely we’ll see anywhere near the start-up entertainment delivered roughly between 1979 and 2000. The wild west days are over.

Take A Gander At A Few Of The More Exciting Post-Deregulation Start-ups. Over the past few years, we’ve constructed a brief and admittedly somewhat irreverent review of the most exciting 35 failed attempts at starting airlines since 1978.

Small Community Air Service Grant Program

The DOT has advised us that the docket for the 2018 Small Community Air Service Development Grant program (SCASD) won’t be issued before Christmas.

That means that the 2018 program will likely be in 2019… Gives an indication of the level of importance the program holds at the DOT.

In the meantime, if your community is considering filing a grant application, click here for our Guide To The SCASD Program. We’ve won more SCASD grant dollars than any other consulting firm.

Monday Update – December 10, 2018

Four Decades of Airline Deregulation

We discuss the disappearance of the independent regional airline industry, and how a lot of small communities are getting hornswaggled by “studies” done by the equivalent of shady used car salesmen… that only keep them from moving into the new communication future…

On December 15, 1978, the government shackles started to be removed from the airline industry.

It was gradual at first, but by five years in, say, 1983, the US airline business was booming.

Let’s take a look…

Nowhere was this more evident than in the regional airline industry … there were over two dozen such small airlines… most were flourishing with their own independent brand identities, route systems and market turf.

Guys In Plaid Jackets Galore. It was boom time for these companies – and for manufacturers of “regional airliners.” At the industry’s annual tribal festivals, a.k.a. conferences of the Regional Airline Association, any attendee with more than a ramper’s title at a “commuter airline” didn’t have to worry about dinner or drinks. Just find one of the phalanx of aircraft sales people and introduce yourself.

This part of the airline business was enjoying huge growth, and so we had the perfect match – airlines looking for deals on new flying machines, and a host of aircraft manufacturers ready to deal – some not too unlike the archetypical plaid-jacketed denizens from rural used car lots.

Invites to fancy meals and lavish “meeting suites” were open to just about anybody with an airline ID. Wine’em, dine’em and sign’em.

There was Beech, Casa, Piper, Fokker, Embraer, Fairchild, BAe, Dornier, Cessna, ATR, Saab, Shorts, deHavilland, all with teams circulating like hungry barracudas to schmooze with the independent “regional” airlines in attendance. The pitch was simple: buy a really great new fleet of Piper T-1040s or Casa 212s and get the jump on your competitor that’s still flying those dumpy old A-model Beech-99s.

And, E-Z financing, too! No cash? No worries! Some of the finance programs were directly from plaid-jacket land.

Lotsa customer targets, too… Fish in a barrel. There was Cascade, Air Oregon, Precision, Rio, Chaparral, Bar Harbor, PBA, Permian, SwiftAir, Southern Jersey, Air Vermont, Atlantis, Down East, Royale, Inland Empire, Air New Orleans, Mesa, Mesaba, Gem State, Aeromech, Big Sky, Golden Gate, Command, Simmons… just for starters… most of them looking for airplane deals.

Again, all of them had their own independent route systems and brand identity. All were expanding and were looking to morph into something bigger. There was no end to the growth of this segment. Small community air service was the future!

Now, while many of these small airlines were well-managed, there were others that were, well, not all that kosher, operationally or financially.

But that didn’t make no nevermind when it came to selling airplanes.

In some cases, the deals included that each new 19-seater would arrive from the factory, replete with a with a check for a quarter or even half million bucks so the airline would have the gelt to get the plane on their certificate – or, maybe, just make the next payroll. It all got blended into the financing.

The future was growth – for not only these “regional” carriers, but for the major carriers, too. No clouds on this horizon.

That Was Just The Start… The Rest Is Less Glitzy. Now, let’s fast forward to today… the deregulation process has continued.

But, unfortunately, most of the airline players so excited about the future in 1983 have not continued. Most of those manufacturers are gone.

So too, with the customers they were pitching back then. But, with the decline in airline players, there’s also a continuing decline in the market for corollary services and support, too. And that process is not played out, yet.

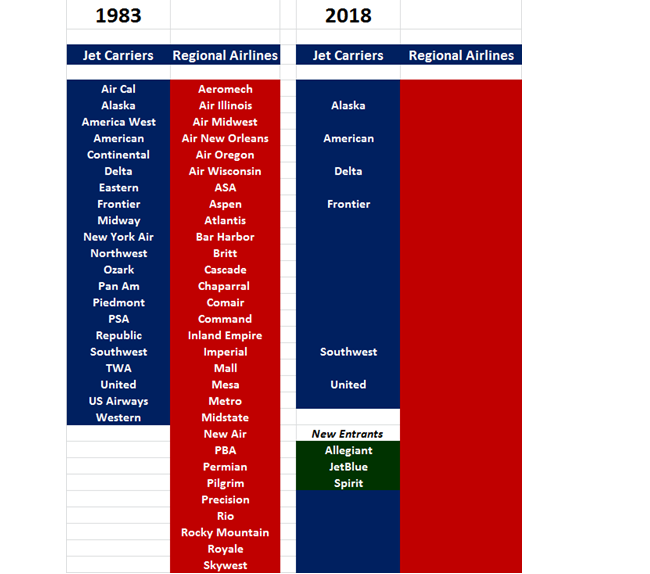

Here’s a quick chart we use to inform communities and airports of the new challenges in “luring” more airlines to town.

The “regional” list from 1983 is not complete, but it gets the point across… not only have those airlines disappeared as independent brands (and most as live companies) but the entire industry that once gathered at RAA conventions is gone too. There is no independent regional airline system, with defined market turf and concrete route systems. It is gone, just like the C-99s, Metro-IIIs, Shorts-330s and the rest of the hundreds of airplanes they once operated.

We could get into the how’s and whys, including some really bone-headed and actually dishonest decisions from the DOT that helped end the existence of independent regionals, but that won’t change the fact that this industry is vapor.

Plus, the major airline sector is also down to just nine major operators… plus Sun Country now entering the ULCC segment.

More Deregulation-Fallout Consolidation Coming In Other Aviation Areas? The decline in airliner players has also consolidated not only the airframe industry, but suppliers across the aviation spectrum.

Related to that, here’s a fact that gets missed way too often when an airport looks to recruit more service…with just these carriers left, there are no airline mysteries, anymore.

Every airline left on this chart has its own strategy, its own fleet mix, its specific route capabilities. Plus, it’s own general turf… the wild expansion seen in the first five years after deregulation is long over. From that, it’s not rocket science to identify which airline systems might have potential to add service (or, conversely, drop service) at a given airport.

Paying To Study The Obvious… That means no giant “true market studies” or “drive capture analyses” or other voodoo translated into giant 80-page documents will change what’s obvious 99% of the time right from the start regarding which airline system might have interest in expanding to a given airport. Airlines have solid market plans… they don’t need some mamaguy consultant studies to tell them their business. (Google it, if you must.)

Or, incredibly, the money still being tossed out at some small communities to simply do studies to find “scheduled flights” – with no first focus on what they may accomplish or whether consumers would use them in light of other travel options, or whether there is actually an airline that could deliver such service – is usually nothing less than buying snake oil. At some point that well is going to go dry.

So it’s amazing – and future-instructive – to see unwary communities get zapped with these expensive rituals, without any prior identification of which of the few airlines left actually can be in the play.

Rural America: A Great Future. As we noted last week (it’s now in the archives), communities of all sizes need to focus on programs to build and enhance global access. That’s a whole lot more than trying to chase the few airlines that are left to fly to airports they can’t profitably serve. It means comprehensive regional planning – involving all modes of communication and logistics. Scheduled flights at the local airport is just one thread – and one that’s no longer economically viable in some cases.

At Boyd Group International, we help our clients focus on future opportunities emerging from the new sets of communication and logistics modalities. Air service is just one of these – and it’s one that has entirely different dynamics than even ten years ago. New approaches consistent with the shifts in the global economy are imperative.

Airline deregulation is just one part of the shift in global communication. There are new opportunities in line.

But in the meantime the plaid jackets are still in evidence – at least for now.

At some point, this myopic pied-piper business is going to consolidate, too. Another victim of deregulation, actually.

A positive one.