Happy New Year!

The Southwest “Point-to-Point” Lore

Facts v Trendy Assumptions

In the media din surrounding the Southwest Black Holiday fiasco, the usual suspects on the margins of aviation knowledge have come out with all sorts of prognostications regarding the reasons for the meltdown.

One of the trendiest is the suggestion that Southwest’s point-to-point system was a contributor to the complexity of the operational collapse. The rationale given doesn’t make much sense, except to illuminate the lack of expertise of the authors.

One reason is that Southwest isn’t really a point-to-point carrier.

Nope. Sorry to shatter dogma, but WN actually depends on connecting (“flow”) traffic as a major part of its revenue generation. Not a sideline, but a fundamental part of its system.

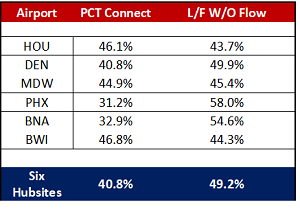

Let’s  look at the traffic mix – local O&D and connect – at six of Southwest’s largest operations for the 12 months ended 3Q 2022:

look at the traffic mix – local O&D and connect – at six of Southwest’s largest operations for the 12 months ended 3Q 2022:

Sorry to rain on the veneer analysts’ parade, but at these airports, the connect flows are a significant and very critical component of the Southwest revenue passenger mix.

Underscoring this is the column on the right. It indicates what the WN load factor would have been without the connect traffic. In short, Southwest is operating these airports as connect points.

In the real world, that’s called a hub operation.

Point: WN may or may not actually schedule in specific banks (we are splitting hairs here) but at these airports, they are in business to aggregate traffic across their system, i.e., connect passengers.

The reality is that Southwest really is a network carrier. True, it has a cohesive fleet of 737s – 700/800 and Max8s, instead of a wide range of capacity units. This limits the mission applications and markets it can pursue. (Although it is more lore that they’ve always operated “one airliner.” They may look alike but the 737-700 and the 737-8 (Max) have a lot not in common. Plus, in at least two time periods, they operated 727s.)

But in places like Tucson, the ability to flow passengers over Houston or Denver Midway is essential for Southwest. In fact, Southwest lists as many as ten flight options between Tucson and Atlanta – every one being a connect itinerary.

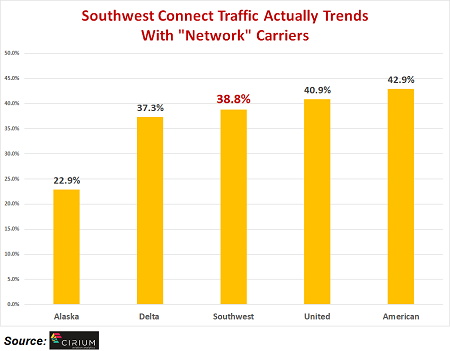

Actually, Delta Is More Point-to-Point Than Southwest. Here’s where the facts get in the way of trendy lore. Take a look at how Southwest ranks v other airlines in regard to percentage of passengers making connections.

We tossed in Alaska just for reference. The data are clear. The Southwest system is essentially as connect-focused as are American, Delta and United, and if international traffic flows were culled out, it’s likely all four are neck-and-neck in regard to percentages of flow traffic.

We tossed in Alaska just for reference. The data are clear. The Southwest system is essentially as connect-focused as are American, Delta and United, and if international traffic flows were culled out, it’s likely all four are neck-and-neck in regard to percentages of flow traffic.

Not to be missed is that Delta actually has a larger percentage of point-to-point traffic than does Southwest.

The hard reality is that the Southwest system – large capacity airliners of 137 to 175 seats – needs strong aggregation of traffic flows.

So, do be circumspect when the media gurus and inhabitants of hobbyist aviation websites spout the lore about WN being “point-to-point.”

At some key airports – like LGA – the traffic is almost entirely point-to-point. But without the revenue flows generated at their hubs such as HOU, DEN, BNA, MDW, etc., they would not be in business.