The New Role of International Traffic –

Affecting Airports Across USA In 2023

We need not touch too much on the fallout of EU airports as they evolve into competition with Ringling Brothers.

Key connect points like Heathrow and Amsterdam have become three-ring circuses. ‘Cept instead of trained bears and performing elephants, they’re making the audience – passengers – the main attraction.

The assumption in the media seems to be that it’s all due to a crush of passengers. A crush there is, but the real reason is that a number of airports are simply under-staffed and poorly-managed.

The assumption in the media seems to be that it’s all due to a crush of passengers. A crush there is, but the real reason is that a number of airports are simply under-staffed and poorly-managed.

A Ouija Board isn’t required to divine the fallout this has on trans-Atlantic traffic flows. What a life experience it might be for the family of four stuck, in a crowd at LHR, with their flight to Rome cancelled and their checked luggage dispersed across Europe like post-war Care packages. Truly character-building for the kids.

The trans-Atlantic boom has become the trans-Atlantic Gong Show.

But that’s not the only place where the traditional contribution of international travel will fall short.

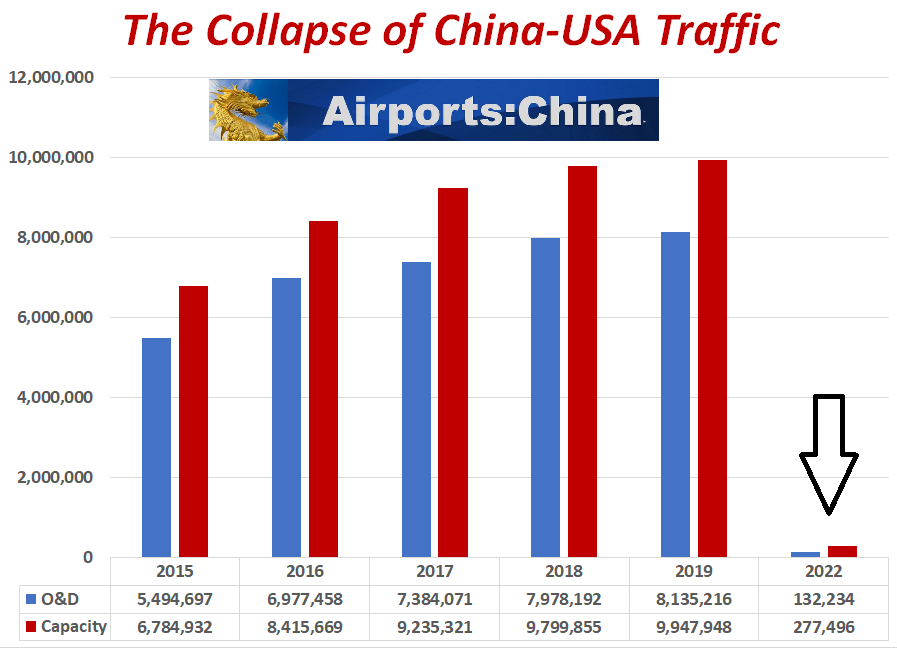

For those on our weekly Touch & Go™ newsletter distribution, we’ve recently outlined the fact that USA airports since 2018 have seen a decline of approximately 8 million annual O&D passengers in one international travel segment alone.

Poof. Gone. Not coming back. Not just a declining travel sector – a vaporized travel sector.

It’s the USA-China market. Here’s a tidbit, according to data from our friends at Cirium, today, the second largest (albeit very shaky) global economy now has less that one fifth of the nonstop traffic from the US than does Turkey. Actually just over 16%.

As we noted in the T&G, China leisure visitation accounted for over 6 million of the 8 million O&D in 2018… that’s around 3 million tourists. And they were not shrinking violets after they got through customs. Based on Airports:China™ research, the total “spend” was over $15 billion dollars. Tour companies took these folks to points all across the nation. Not anymore. We touched on examples of places that are being materially affected by this change.

There are a lot of dynamics in play here. The politically-trendy dodge is the supposed “trade” war between the two countries. The real reasons are internal political shifts in China, like, faltering Chinese economy, billions caught in Ponzi-like real estate scams, a run on the banks, the CCP-created and continuing Covid pandemic, and – trade war or not – the hard fact that the CCP is now actually restricting all foreign travel. Outside of the flashy skyline of Shanghai’s Pudong, the place is a house of cards.

There’s more than the tourist component. The chaos in the business sector is indicative of a wider challenge well beyond just seats occupied on trans-Pacific airliners. The message here is that the once-robust Chinese investment in the USA is dead. Gone. No more.

It also points to the need for looking at the fallout due to potential changes in US regions where there has already been strong investment from companies in the Middle Kingdom. Where these head will make economic waves that can and will affect disposable and business spending on air travel.

Regardless of other issues, the Chinese economy is heading south. That means Chinese companies are heading that way, too.

The deterioration of diplomatic relations also puts in question the future direction and status of the economies of US regions with high dependence on Chinese-owned businesses. If the mother country is in economic decline, and the government is in policy-confusion, that probably will have an effect on the future of Chinese owned companies already established in the USA, too.

Remember, every Chinese company – every one – involves the heavy hand of the CCP, the mafia that runs the country. As they make decisions regarding the relationship with the US, it can and will affect the direction of China-owned companies operating here.

There are obvious examples. Raleigh-Durham comes to mind, with the extensive presence of Lenovo. So does Louisville, where the former General Electric appliance factories are actually owned by Haier of China, and the brand “GE” is being used for an agreed pro-tem period of time.

But there are many others. Locations where, say, Smithfield Foods (owned by China) has processing facilities. There are auto parts factories in Michigan owned by CCP-controlled firms. There are dozens of such examples.

How these communities will be affected is not clear, and will depend on a range of factors. But they will be affected, and that will shift the direction of long-term traffic demand patterns, both domestically and internationally.

Summary: The point is this. The role of international travel demand within airport and aviation planning is changing. Pre-pandemic, international demand generated – directly and indirectly – almost 32% of enplanements at US airports. Naturally, that affected JFK and SFO a lot more than MBS or GEG. But it was a factor.

It still is… except Airports:USA® forecasts indicate this percentage will be closer to 20% in the immediate years ahead. The situation in the EU is likely shifting leisure attention to Hawaii, Mexico and other more stable destinations. China is now a hermit kingdom. Other points in Asia are not in line to replace this lost traffic.

Add In New Fleets, And Travel Patterns Will Change Even More. BGI has often pointed out that new-generation airliners such as the A220-300 and the A321XLR will open new international (mostly trans-Atlantic and LatAm) markets at large, non-hubsite secondary US airports. Albany, Grand Rapids, Richmond and at least half a dozen more airports will be in the crosshairs of EU carriers seeking to expand their hub operations on the Continent. Assuming there is airport capacity.

Put that into the research mix, and the name of the future airport planning game is to be completely outside the traditional planning box.

The conclusion is that all air service planning should discount the past and make assumptions about the new future – domestically and internationally.

It’s still a global economy. It’s just a very different globe.

______________________

By the way, if you’re interested in joining the aviation professionals who receive our Touch & Go Newsletter at the end of each week, just click here.

By the way, if you’re interested in joining the aviation professionals who receive our Touch & Go Newsletter at the end of each week, just click here.

_______________________