The Plot Thickens…Airport Planning Take Note

Now, A Fourth US Carrier Suffers Parked 737 MAX Fleets…

… and All Four Are Affected Differently.

Boeing 737 MAX 8, S/N 44079, has taken its place in an aircraft parking lot somewhere in North America. A second unit, S/N 44080 will be there shortly, too.

With that, Alaska has now joined American, Southwest and United in having its fleet plan affected by the grounding. These are the first of five scheduled for delivery this year to the airline.

Now that it may be the New Year before the MAX fleet is back in the sky, let’s cut to the bottom line regarding what airports can expect in regard to air service shifts.

A Financial Hit. Not A Torpedo. None of these carriers are facing any financial danger as a result of not taking on the numbers of MAX airliners planned. Their “hit” is that they could be filling these extra airplanes, as well as gaining some efficiencies in operations.

Fleets Are Still Growing – With One Exception. Also, all four of these airlines will be operating fewer departures than planned, but that does not translate necessarily into less flying than a year ago, nor cancellations in the retail consumer sense.

The flights just won’t be in the schedule, and those passengers that may have been in for long-advance bookings face the same resolution as when routine schedule changes affect operations. They generally get rebooked.

Most of AA/UA System Departures Are Not Directly Affected. Today, less than half of all United and American branded system flights are actually operated by these carriers. The rest are outsourced to entities such as SkyWest, Trans States, Air Wisconsin, etc.

Over 55% of United-branded flights are operated by other than mainline United, and almost one third of departing seats are there, too. Numbers are very similar at American.

Only Southwest doesn’t have any other new aircraft coming into its fleets… AA, UA and AS all have other aircraft on order, and being delivered, both mainline and to outsourced lift providers.

AA and UA are accepting previously-ordered Airbus aircraft, and both continue to be actively adding used A-319s. Plus, they are also placing mainline-cabin E-175s, many owned and leased out to outsourced operators such as SkyWest.

They are also continuing to add widebody aircraft – new and used. United recently completed taking 767s formerly operated by Hawaiian. 787-10s are coming on line, too.

Point: The MAX grounding is a giant financial headache, but will not cause chaos at the nation’s airports. However, that could be the operative word in front offices when it comes to determining the potential revenue being forgone at the four affected airlines.

American Airlines

They had to park 24 active aircraft in March, and not take delivery of an estimated 16 more since then. Previously-planned deliveries would indicate that by the end of the year, American will not have the services of approximately 55-60 737 MAX airliners.

They currently operate a narrow-body fleet of approximately 725 airliners (not including 757s), assuming that the last MD-80s are retired. There are no strong indications that, other than 20 E-190s, any major part of the current fleet may be in line for near to mid-term retirement.

Therefore, beyond filling some of the MD-80 gap, most of the new MAX capacity was likely to contribute to new additional revenue generation. But it isn’t a situation that stops the airline in its tracks. The airline has a solid 117 A-320/321s on firm order, plus the E-175s continuing to be placed at surrogate operators.

Prognosis: AA will likely continue to re-think any near-term expansion – re-think, not necessarily eliminate.

United Airlines

The airline has 14 MAX-9 airliners parked with another 151 of all categories – 8,9,10- on order. This is within a current narrow-body fleet of 494 airliners. As time passes, these missing deliveries will become more apparent in the carrier’s route planning.

However, as with American, 55% of the United-branded departures are not affected directly, as they are operated by outsourced “regional” (misnomer) partners.

Prognosis: United, like American, is actively adding used A-319s to its fleet, but these are essentially a dribble in regard to new capacity. Assume that any expansion or capacity additions involving narrow-body flying will shift to a back burner for the near term.

Southwest

With only 737 MAX airliners on order, Southwest faces a situation where any new expansion will be very tough to accomplish until the situation is resolved.

They have 291 MAX units ordered, including the 34 that were taken out of the fleet. The airline does not have a “regional” (misnomer) set of operators to which to shift any capacity.

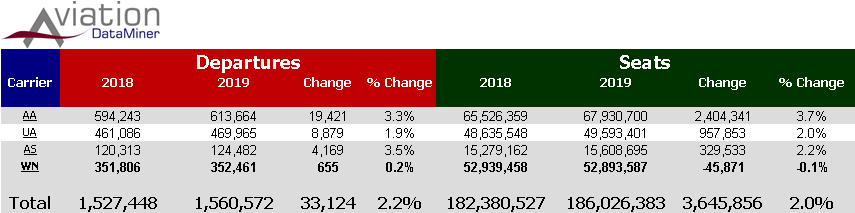

The limited options for Southwest are illustrated when we look at the capacity planned for the three carriers July through September

Alaska, United and American have some alternative fleet flexibility to take advantage of the growth in air travel due to the strong economy.

Southwest has less, and is holding the line compared to last year. It is likely that any retirement of -700s that may have been contemplated will be postponed– to the maximum extent possible, based on overhaul cycles.

It is likely that the anticipated domestic expansion of WN in late 2020 will likely be delayed into 2021. In addition, depending on how long this fleet-deprivation continues, the carrier will probably sharpen route-planning pencils in regard to current markets.

Bottom Line – Digesting Fleets, Post-Grounding

As it stands, AA, AS, UA are facing the frustrating situation of seeing new revenue and not being fully able to tap it. But they do have expansion aircraft in the pipeline.

Southwest will be marking expansion time for the next six months.

Further, digesting these airplanes when the FAA releases them will not be immediate.

Taking on a couple dozen or more 737s all at one gulp isn’t possible – it will take weeks.

The real winners in this will be flight simulator facilities… remember, when the FAA gives the go-ahead, there literally will immediately be hundreds of airliners ready to fly… and it’s very likely that demand for sim time will be standing room only. And as for MAX-specific simulators, there are currently less than 25 in the world.

Every department at the affected airlines will be in full metal jacket mode.

______________________

Post-Script – China & The MAX – Capacity Relief?

This MAX delay may not be totally unwelcome in China.

As of today, there are approximately 300 MAX airliners ordered by Chinese entities. The delay in deliveries may be a benefit, as it is beginning to appear that historic growth rates are falling in line with the decline in China’s GDP growth – and other issues.

Boyd Group International is now completing the 2019-2020 Airports:China™ forecast of traffic in the Middle Kingdom, covering each of the top 200 airports in the nation. There are some very interesting revelations.

Yes, there is huge latent demand for air transportation… but with the economic downturn in China (and, a lot has not been accurately covered due to media-spin regarding the “trade war”) nationwide passenger growth is slowing materially to under 8% and maybe lower – that’s from well over 10% for the last decade.

Yes, there is huge latent demand for air transportation… but with the economic downturn in China (and, a lot has not been accurately covered due to media-spin regarding the “trade war”) nationwide passenger growth is slowing materially to under 8% and maybe lower – that’s from well over 10% for the last decade.

One of the other forecast issues is secondary Chinese airports, where load factors are not as strong as in the top 25 commercial centers. In fact, the domestic Chinese airline system is in some areas woefully mis-fleeted, with a focus on 737/A320 narrow bodies, when many of the emerging airports cannot support such capacity.

It is interesting that China has very few small airliners in its fleets. The native 76-seat ARJ-21 is becoming a challenge if not an embarrassment – 18 in operation since it rolled out more than ten years ago. ATR has been able to place some -42 turboprops, but only with onerous capacity restrictions. The locally-produced MA60 and MA600 platforms are not widely used in China itself. Nor elsewhere.

The conclusion is that China needs to re-fleet domestically. More 160-180 seat airliners can be placed, but when many airports of under roughly 5 million passengers are seeing load factors in the 65% -70% (or less) range, and which need Beijing government and provincial financial support, a delay in acceptance of several dozen MAX airliners may not be any economic hit to China.

The Airports:China™ forecast is now being completed, with highlights to be posted shortly at www.BoydGroupChina.com, and full details to be outlined at the 24th International Aviation Forecast Summit in Las Vegas, August 25-27.

The Airports:China™ forecast is now being completed, with highlights to be posted shortly at www.BoydGroupChina.com, and full details to be outlined at the 24th International Aviation Forecast Summit in Las Vegas, August 25-27.

The Summit is the only forum that actually is focused on aviation forecasts – trends, dynamics, traffic growth, fleets, and airline strategies. It is also the only event with independent US enplanement trend forecasts, too. Clear discussions and unscripted Q&A with airline and aviation CEOs and senior executives.

Lots of networking opportunities, too.

If you haven’t registered yet, we’d suggest you click here and take a look. Then clear your calendar and join your colleagues at the IAFS.

______________